Biofuel Bunker Snapshot: Rotterdam and Singapore prices decline across the board

FuelEU Maritime triggers biofuel bunker demand

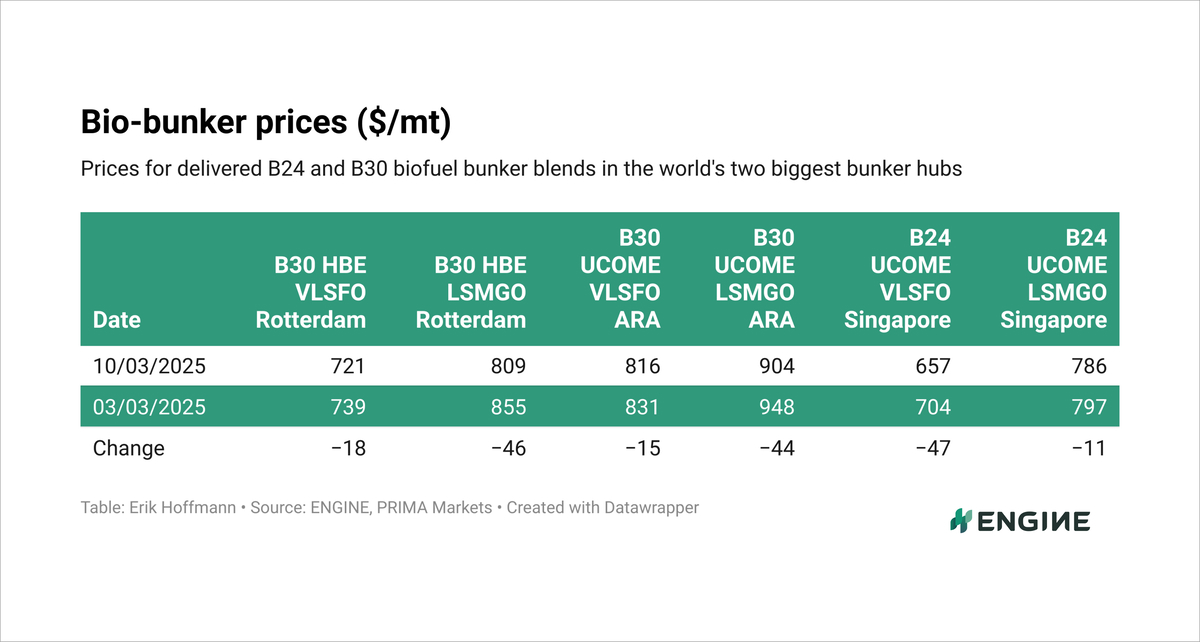

Bio-bunker prices sharply down with lower oil prices

Singapore allows more ships to deliver B30 blends

Rotterdam

There is generally more interest in biofuels now that the EU’s FuelEU Maritime regulation is in play. The regulation penalises ships running on marine fuels with a higher greenhouse gas (GHG) intensity than 89.34 grams of CO2-equivalent per megajoule (gCO2e/MJ) from this year.

The GHG intensities of conventional fossil fuels like VLSFO, LSMGO and HSFO are higher than that threshold by default. By contrast, sustainable biofuels produced from feedstocks like palm oil mill effluent methyl ester (POMEME) and used cooking oil methyl ester (UCOME) tend to be comfortably below that threshold.

FuelEU’s pooling mechanism allows transfers of compliance surpluses from overcompliant ships running on B30 blends or pure B100 biofuel to undercompliant vessels. With compliance deficit penalties and estimated pooling values baked into conventional and biofuel prices – as you can see in our Fuel Switch Snapshots – bunkering biofuels have started to make sense to a lot more shipping companies.

Looking at the biofuel bunker market in the past week, the biggest price drop has come from Rotterdam B30-LSMGO HBE, which has fallen by $46/mt. This has been driven by a $44/mt drop in ENGINE’s Rotterdam LSMGO price, which has put significant downward pressure on the biofuel blend. Although PRIMA Markets’ POMEME CIF ARA assessment - which makes up 30% of the benchmark price - has risen by $45/mt, this has been not enough to offset the LSMGO decline.

A $7/mt increase in PRIMA’s HBE rebate for B30 blends sold in the Netherlands has also helped push the Rotterdam B30-LSMGO HBE price lower, as a bigger rebate effectively reduces the final price.

Rotterdam B30-VLSFO HBE has also fallen, down $18/mt, with its main driver being a $23/mt drop in Rotterdam VLSFO. A massive $45/mt increase in PRIMA’s POMEME CIF ARA has provided some offsetting pressure, while the higher HBE rebate has contributed to the downward movement.

Prices for ARA B30-VLSFO UCOME and ARA B30-LSMGO UCOME have dropped by $15/mt and $44/mt, respectively, largely due to declines in Rotterdam VLSFO (-$23/mt) and Rotterdam LSMGO (-$44/mt). The PRIMA-assessed UCOME FOB ARA price has edged up by $4/mt, providing slight resistance to the downward trend.

Singapore

Singapore has also seen declines, though to a lesser extent than Rotterdam. Singapore B24-VLSFO UCOME has fallen the most, down $47/mt, driven by a $34/mt drop in Singapore VLSFO. The B24-VLSFO UCOME price drop has come despite a $10/mt increase in PRIMA’s UCOME FOB China assessment, which has helped cushion the fall. A $0.75/mt decline in China-Singapore UCOME freight should have had an downward effect on the price, but it has been too small to counteract the overall downtrend.

Singapore B24-LSMGO UCOME has been more stable, falling by $11/mt, as Singapore LSMGO has declined by $18/mt but has been supported by a $10/mt rise in PRIMA’s UCOME FOB China assessment and the slight drop in China-Singapore UCOME freight.

Singapore-registered bunker vessels are now allowed to carry and deliver stems with up to 30% (B30) biofuel. The Maritime and Port Authority of Singapore (MPA) has decided to implement the International Maritime Organisation's (IMO) interim guidance on biofuels early.

This is poised to shake up the Singapore biofuel bunker market, as only some bunker suppliers have been able to deliver blends above 25% biofuel, and have defaulted to 24% (B24) blends to err on the safe side of the hard 25% limit. Vitol and Fratelli Cosulich are among the suppliers that have invested in IMO Type II chemical tankers, which are allowed to carry up to 100% (B100) biofuel.

By Erik Hoffmann

Please get in touch with comments or additional info to news@engine.online