Biofuels are making waves

As a growing part of the shipping industry is exploring ways to trim its carbon footprint, the ENGINE team reports that biofuels are making waves and finding their way to bunker ports around the world.

PHOTO: The Seanergy Maritime-owned MT Friendship receiving a B10-VLSFO blend from TotalEnergies in Singapore last year. TotalEnergies

PHOTO: The Seanergy Maritime-owned MT Friendship receiving a B10-VLSFO blend from TotalEnergies in Singapore last year. TotalEnergies

We often get asked variants of the question: "Where can we bunker biofuels?"

For every region and port that was enquired about, we had to investigate what was available. As the information accumulated in leaps and bounds, we decided to launch a project to map out all the physical bunker suppliers that offer biofuels in more and more ports.

It’s a moving target, and this is some of what we have uncovered so far.

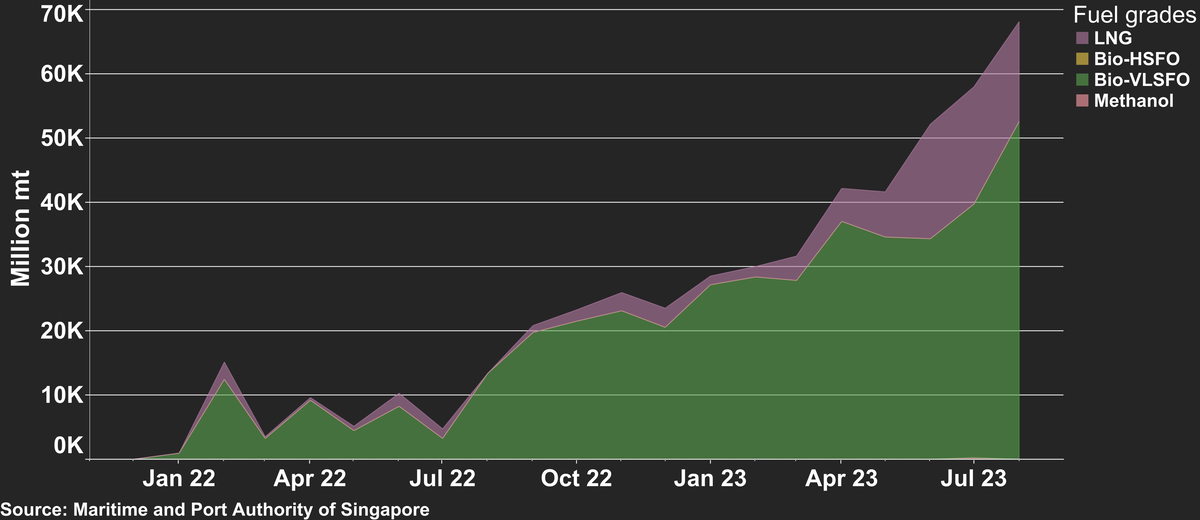

East of Suez

CHART: Biofuel blends still only make up a fraction of Singapore’s total bunker sales, but coming from a small base, bio-blended VLSFO sales have hit the 50,000 mt mark for the first time. Maritime and Port Authority of Singapore

CHART: Biofuel blends still only make up a fraction of Singapore’s total bunker sales, but coming from a small base, bio-blended VLSFO sales have hit the 50,000 mt mark for the first time. Maritime and Port Authority of Singapore

Biofuels are starting to become more common in Singapore, but so far they have only made up a fraction of the port’s total bunker sales. B24 (24% biofuel) is the standard blend ratio as sea-going bunker barges are restricted to carrying 25% biofuel and as suppliers seek to err on the safe side of that requirement. Prices are often quotes as a premium over very low sulphur fuel oil (VLSFO) and the typical biofuel grade is fatty acid methyl ester (FAME), which is also called biodiesel.

A couple of Chinese bunker suppliers have started offering biofuel blends for delivery in Zhoushan and Guangzhou, and another two have brought them to Hong Kong. As biofuel blends don’t qualify as bonded bunkers in mainland China, in which value added tax (VAT) is waived for VLSFO, it makes less sense for Chinese refiners and blenders to blend them with VAT-exempt VLSFO. The suppliers therefore import finished B24-VLSFO blends from Singapore and other places before they are sold in Chinese ports.

B35-MGO blends are available in Indonesian ports because of a national 35% minimum biofuel blending mandate. But these derive from palm oil and are not sustainable. Palm oil’s close connection to deforestation means they won’t qualify under the International Sustainability and Carbon Certification (ISCC) programme or as renewable fuels towards upcoming European Union (EU) regulations.

In the Middle East there is one major producer and wholesaler of waste-based biofuels. The UAE-based producer has struck supply deals with two physical bunker suppliers in the country, where it collects used cooking oil (UCO) from McDonalds restaurants and other sources. One of the suppliers has so-called ISCC-certification, which requires the biofuel to meet certain sustainability criteria throughout its lifecycle. From a small base, the producer says that bunker demand has doubled in each of the past three years, and that demand is expected to grow exponentially in the years to come.

Europe & Africa

CHART: Total biofuel sales have increased from 149,000 mt in the first quarter of this year, to 186,000 mt in the second quarter. About 78% of the biofuel blends sold in the second quarter were bio-VLSFO, followed by bio-HSFO (14%) and bio-MGO (5%). Port of Rotterdam

CHART: Total biofuel sales have increased from 149,000 mt in the first quarter of this year, to 186,000 mt in the second quarter. About 78% of the biofuel blends sold in the second quarter were bio-VLSFO, followed by bio-HSFO (14%) and bio-MGO (5%). Port of Rotterdam

Rotterdam dominates the global biofuel bunkering scene. Around 6% of all of the bunkers sold in the first half of this year was blended with biofuels, and that was down from an even stronger 8% last year. More biofuel trials and regular refuelling of ships have taken place in Rotterdam than in any other port and a greater number of suppliers offer biofuels there.

Local biofuel processing capacity, imports from China and competition between bunker suppliers in a burgeoning biofuel bunker market provide economies of scale in Rotterdam and contribute to keep prices in check.

But perhaps the biggest reason behind its growth is simple. Rotterdam is Dutch, and the Netherlands has generous market mechanisms in place for biofuels sold for bunkering, particularly for advanced waste-based biofuels. In fact, the price incentives have worked too well and pulled biofuel feedstock away from the road fuels market. The road fuels market faces tougher blending mandates, and more biofuels are needed to meet them, the government told ENGINE.

To rebalance the biofuel scales between road and marine, the Dutch government has launched a consultation with a proposal that could effectively halve the biofuel rebate multiplier. This could see Rotterdam’s discount of more than $200/mt to Singapore be slashed to about half that.

Mediterranean bunker suppliers are also starting to catch the biofuel wave. A few suppliers across Gibraltar, Spain, Malta and Italy now offer blends. Some typically need a week or two of lead time to source, blend and deliver the fuel to ships. One supplier has struck a deal with a ferry company that has tested biofuels blended in small ratios on a ferry with the upcoming FuelEU Maritime regulation in mind.

A lack of biofuel demand in South Africa and Mozambique has meant that suppliers have so far held back on bringing it to market. Some are saying they hope to pursue biofuel in the future.

Americas

US biofuel bunkering is struggling to gain traction in the absence of government subsidies. While harbour crafts and road vehicles enjoy subsidies, ocean-going vessels do not. This has meant that comparable B30 biofuel blends have been prohibitively expensive in Houston compared to Rotterdam for example.

Unlike Rotterdam and the rest of the EU’s upcoming CO2 and greenhouse gas (GHG) regulations, there are also no nationwide US environmental regulations to incentivise uptake of biofuel blends by ships. Customer demand will therefore likely come from ship types close to the end consumer, like ferries, cruise ships and container ships.

Some bunker suppliers have already announced readiness or intent to offer. These include California, where local environmental regulations have boosted uptake of 99% renewable diesel (R99), which differs from FAME in that it is not chemically esters. Canada’s Vancouver, the US Gulf Coast, Colombia’s Cartagena and Brazil make up some of the other places with biofuels on offer.

The Panama Canal is likely the biggest bunker area in the Americas, but a joint venture of companies that was previously buoyant about the prospect of building at least one biorefinery and importing biofuels for bunkering and other transport fuel markets has more recently cast doubts about its feasibility. "The issue is feedstock and competing with current subsidies in the US and EU markets that hog and distort [the] price of feedstock," one of the companies told ENGINE.

Meanwhile, a recent entrant to the US Gulf Coast’s biofuel bunker market has been championing a mass balancing approach. Its pricing is based on the feedstock type, but thanks to mass balance accounting the feedstock purchased does not necessarily need to be the feedstock in the fuel consumed by that buyer’s ship. Blends based on UCO, soybean oil and tallow are current options, and more waste-based biofuel alternatives is expected to follow in the future.

To help shipowners get more clarity around what’s available where, ENGINE will come out with more detailed overviews of biofuel bunker supply by region and port later this year.

By the ENGINE team: Shilpa Sharma, Nithin Chandran, Queeneerich Kharmawlong, Konica Bhatt, Debarati Bhattacharjee, Aparupa Mazumder, Tuhin Roy and Erik Hoffmann