Correction: Limited biofuel bunker traction across the Americas

There were pockets of biofuel bunkering progress in the Americas last year, but uptake was sparse and highly fragmented.

IMAGE: Petrobras bunkering a vessel with B24-VLSFO in Rio Grande. The biofuel was blended at Transpetro's Rio Grande Terminal. Petrobras

IMAGE: Petrobras bunkering a vessel with B24-VLSFO in Rio Grande. The biofuel was blended at Transpetro's Rio Grande Terminal. Petrobras

Corrections: The comments from a Canada Steamship Lines (CSL) spokesperson did not come directly from a spokesperson at the company, but through an intermediary. This is not good reporting practice and after uncovering it, we apologise. Some of the information about Port Colborne and CSL has therefore been removed.

Other information reported was inaccurate. CSL is not developing a dedicated biofuel terminal in the Port of Hamilton. That is being developed by HOPA Ports. The biofuel CSL has bunkered has been B100, which has around 92% lower CO2 emissions than conventional marine gasoil, not a 23% reduction as previously stated.

It is also important to point out that while ENGINE’s fuel quality lab data represents about 60% of all bunker fuel quality samples, this does not necessarily mean 60% equally across ports. We therefore now only refer to fuel samples in percentages of total samples for individual ports.

Biofuel bunker activity across the Americas accounted for around 5% of global biofuel bunker deliveries in 2025, according to ENGINE’s fuel quality data, which represents approximately 60% of all lab samples globally.

Houston, New York and Panama remain the main options for biofuel bunkering, with some activity also seen in Colombia, but demand on the biofuel side is still fairly sparse, a bunker trader told ENGINE.

A review of biofuel bunker delivery samples across the Americas over the past year shows that activity has been highly concentrated by geography, month and fuel grade, with most ports recording only intermittent deliveries.

US dominates samples, Canada has continuity

By country, the US had the most biofuel bunker lab samples recorded, accounting for about 49% of deliveries in the Americas. Activity was spread across the US Gulf Coast, Atlantic Coast and West Coast, but deliveries remained sporadic.

According to ENGINE’s data, Canada accounted for roughly 28% of total Americas biofuel samples, making it the second-largest contributor by country despite having far fewer bunkering locations than the US.

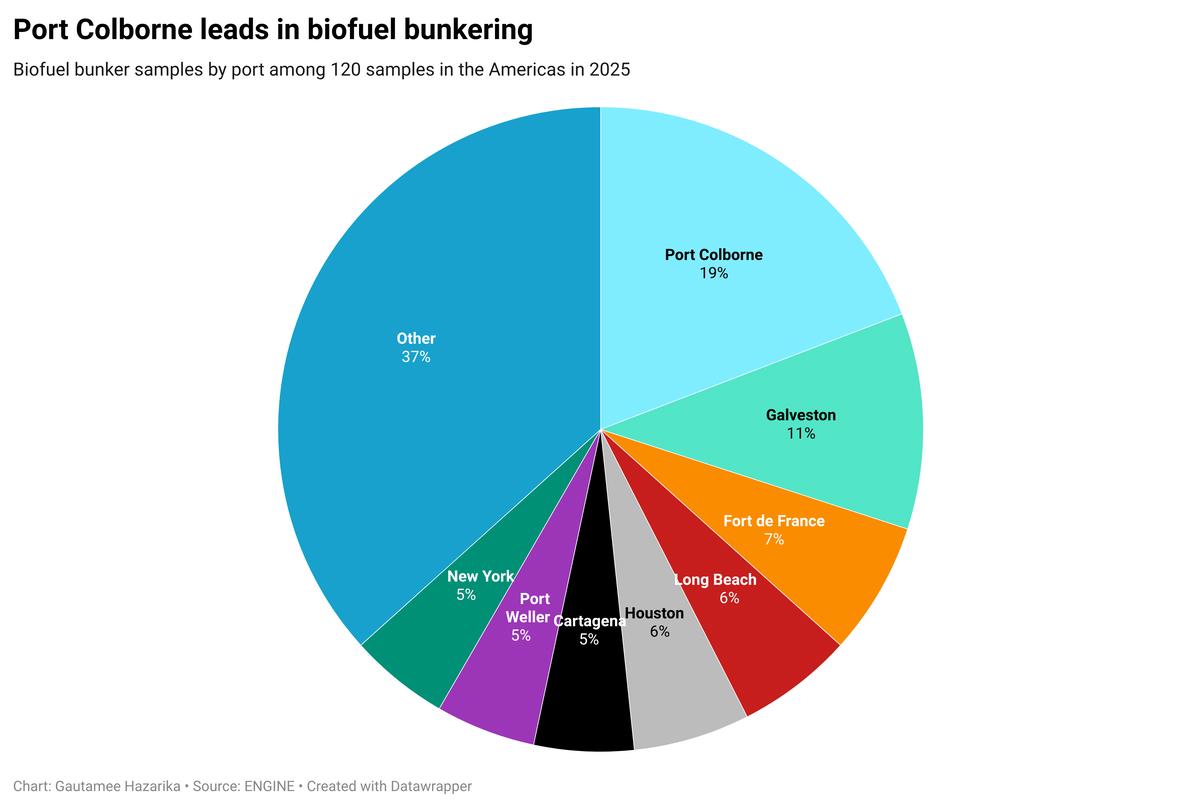

Most of Canada’s activity was centred on the Great Lakes region, particularly in Port Colborne with 19% of Canadian biofuel bunker samples, according to ENGINE fuel quality data.

The Port Colborne Marine Biofuel Terminal was announced back in 2024, which is an 8-million-litre [7,000 mt] biofuel facility being built in Port Colborne, Ontario.

The C$33-million ($24 million) project is being developed by HOPA Ports and Canada Clean Fuels and backed by C$13.8 million ($10.1 million) in federal funding.

At full capacity, the facility will be able to distribute up to 70 million litres/year [61,000 mt/year] of biodiesel, sufficient to fuel more than 100 vessels/year, HOPA Ports has said.

The facility is expected to be completed by 2027.

Canada Steamship Lines (CSL) has been operating about half of its Canadian fleet on pure B100 biodiesel for years now, including eight Great Lakes vessels like the Baie Comeau and Whitefish Bay. This B100 can reduce CO2 emissions by around 92% compared to conventional marine gasoil.

Limited activity elsewhere

In North America, activity was heavily skewed towards a handful of locations, led by Port Colborne, Galveston, Long Beach and Houston, while most other ports recorded only one or two samples over the year, highlighting the early-stage and uneven development of biofuel bunkering across the region.

In the US, biofuel bunker activity was concentrated in a limited number of ports, with deliveries spread unevenly across the East Coast, Gulf Coast and West Coast.

In New York, BunkerOne started offering biofuel blends such as B30-HSFO and B30-LSMGO in May. The B30 blends contain 30% fatty acid methyl ester (FAME) or hydrotreated vegetable oil (HVO) biofuels blended with HSFO or LSMGO. The fuels are sold on ISO 8217:2017 specifications and are ISCC EU-certified.

There were six samples from New York, which accounted for roughly 5% of total biofuel bunker activity in the Americas in 2025.

Colombia accounted for 6% of all Americas samples, driven by samples from Cartagena and Mamonal, while Panama’s Cristobal and Balboa contributed just over 4%. Brazil followed with just over 3%, with activity recorded in Rio Grande and São Sebastião.

Monjasa completed its first ISCC-certified biofuel bunker operation in Cristobal in March.

Only modest biofuel bunker volumes have been recorded on the Atlantic side of the Panama Canal, where Cristobal is the biggest bunker port. Monjasa’s 900 mt biofuel stem in February was the only biofuel to be bunkered last year until October, when sales hit 1,600 mt. That was followed by 2,221 mt in November, while nothing was recorded in December, according to preliminary data from the Panama Maritime Authority.

In Brazil, Petrobras launched biofuel bunkering in Rio Grande at the beginning of 2025, offering B24-VLSFO after securing an ISCC EU certification for its oil and biofuel terminal at the port.

In December, Norwegian chemical tanker operator Odfjell announced the first biofuel-based green corridor between Brazil and Europe. Odfjell will offtake B24 biofuel blends in Rio Grande as a way to secure long-term fuel availability.

In June, Argentina approved biofuel blending for bunkering. However, uptake has been disappointing so far, with ENGINE’s samples not showing a single stem for any ports in Argentina in 2025.

Malcolm Dickson of Antares Ship Agents informed there is a supplier for biofuels in Argentina, from which deliveries can be arranged at certain open berths as they must be made by truck.

“To the best of my knowledge there have been no sales yet,” Dickson added.

Dickson said the supplier does not offer biofuels at Argentina’s popular Zona Común bunker spot. This is primarily because deliveries have to be made by truck, and Zona Comun is an anchorage about 6 miles offshore. Only tankers perform deliveries there and there are no dedicated biofuel delivery vessels.

Pure biofuel in demand

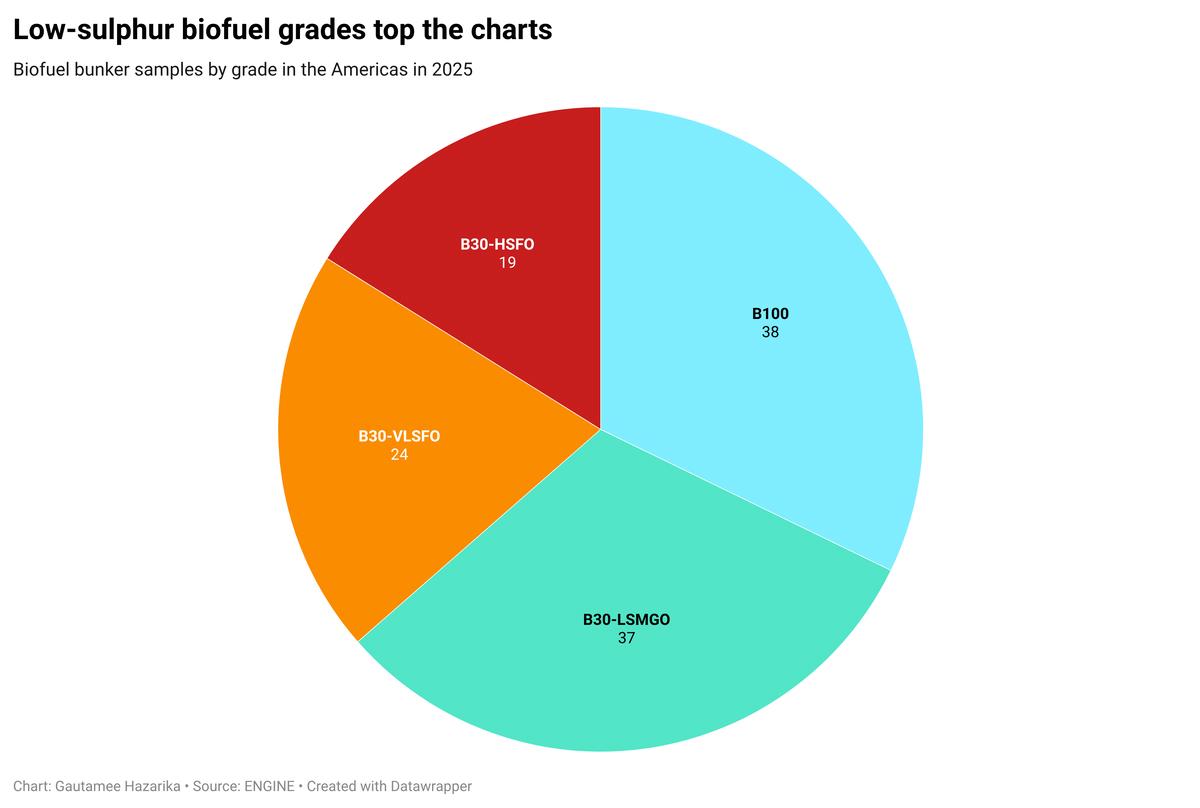

B100 biodiesel was the most popular biofuel grade across the Americas last year, followed closely by bio-LSMGO blends. Both of these grades have less than 0.10% sulphur which make them compliant with the North American and US Caribbean Sea Emission Control Areas (ECAs).

B100 accounted for around 32% of total biofuel bunker samples, while various bio-blends made up about 68%.

Bio-LSMGO comprised roughly 31% of samples, followed by bio-VLSFO at 20% and bio-HSFO at 16%.

Bio-ULSFO remained marginal, representing less than 2% of total samples.

Seasonal biofuel demand

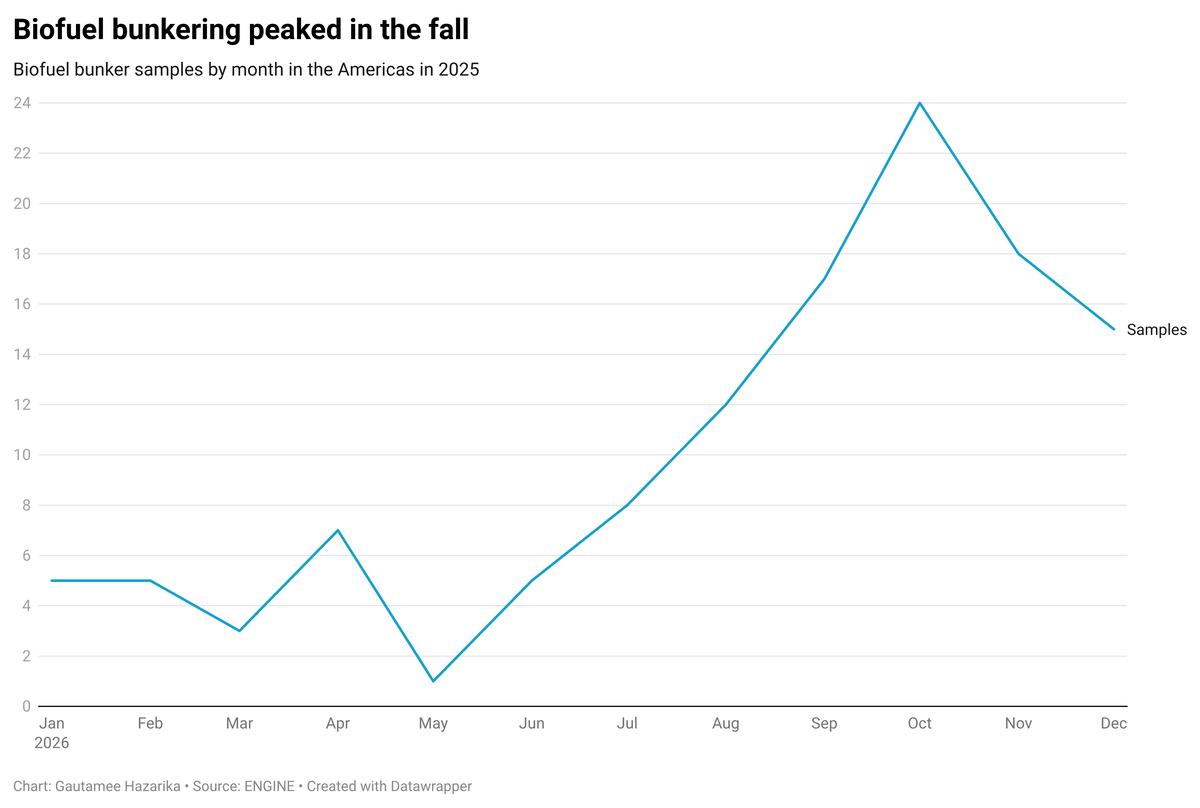

Biofuel bunker activity was seasonal in the Americas, with deliveries heavily concentrated in the second half of the year.

October recorded the highest share of activity with 20% of total biofuel bunker samples, followed by 15% in November and 14% in September.

Together, September–November made up nearly half of all recorded biofuel bunker activity.

By contrast, activity was notably thin during the late spring and early summer, with May accounting for less than 1% of total samples and March contributing just 2.5%.

The seasonality in demand suggests that bio-LSMGO and bio-ULSFO deliveries were tied to specific vessels trialling biofuels rather than routine bunkering, a trader told ENGINE.

Priced out?

Today, high biofuel costs continue to weigh on uptake in the Americas. It has often been cheaper for operators to bunker in established global biofuel hubs such as Rotterdam or Singapore than in ports like Houston and Cristobal.

On certain days last year, suppliers in Houston priced B30-VLSFO $110-223/mt higher in than in Rotterdam, and $60-271/mt higher than in Singapore, according to ENGINE prices gathered from the market. The biofuel grade was also priced at $106-143/mt premiums in Cristobal over Houston, and $116-176/mt over Singapore.

B100 was priced $266/mt higher in Houston than in Rotterdam, and $73/mt higher than in Singapore on one day. B30-HSFO pricing was closer between the ports, with Houston at a $21/mt premium over Rotterdam and $15/mt over Singapore.

While emissions from voyages from non-EU ports in the Americas into the EU are covered under the EU ETS and FuelEU Maritime regulations, ports across the Americas generally lack dedicated incentives or port-level mandates for marine biofuels.

As a result, biofuel bunkering in the region has been shaped more by route-specific compliance considerations and individual operator strategies than by local regulatory or commercial drivers, contributing to uneven and selective uptake.

By Gautamee Hazarika and Erik Hoffmann

Please get in touch with comments or additional info to news@engine.online