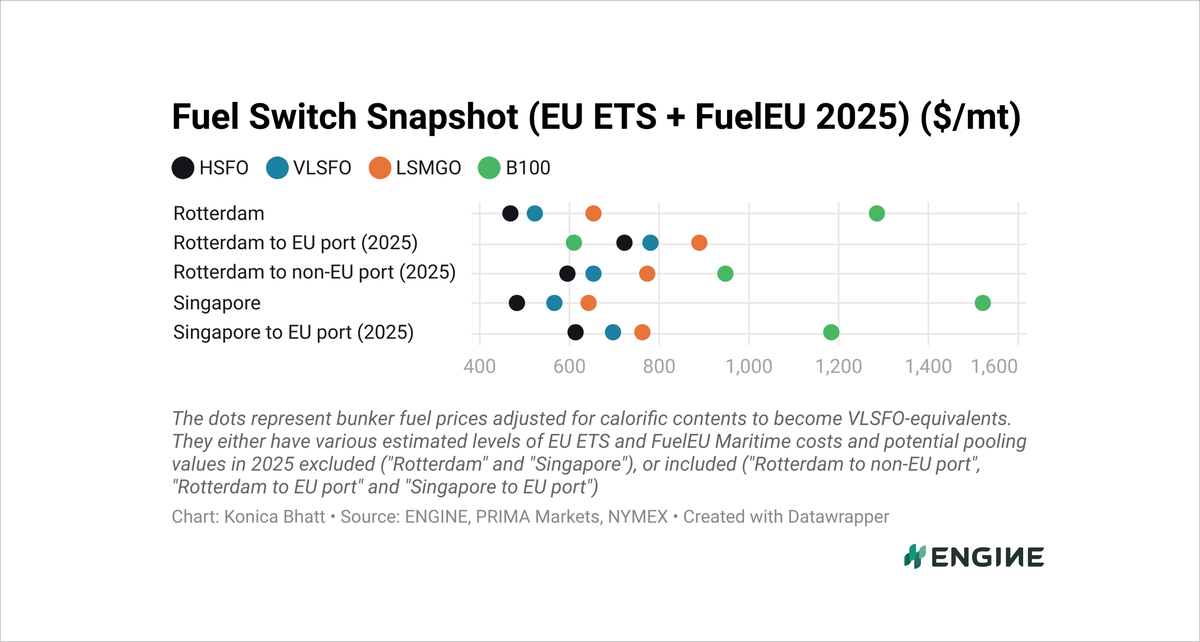

Fuel Switch Snapshot: B100 discount to VLSFO widens

VLSFO climbs on Brent rally

Rotterdam B100 pooling benefit narrows over the month

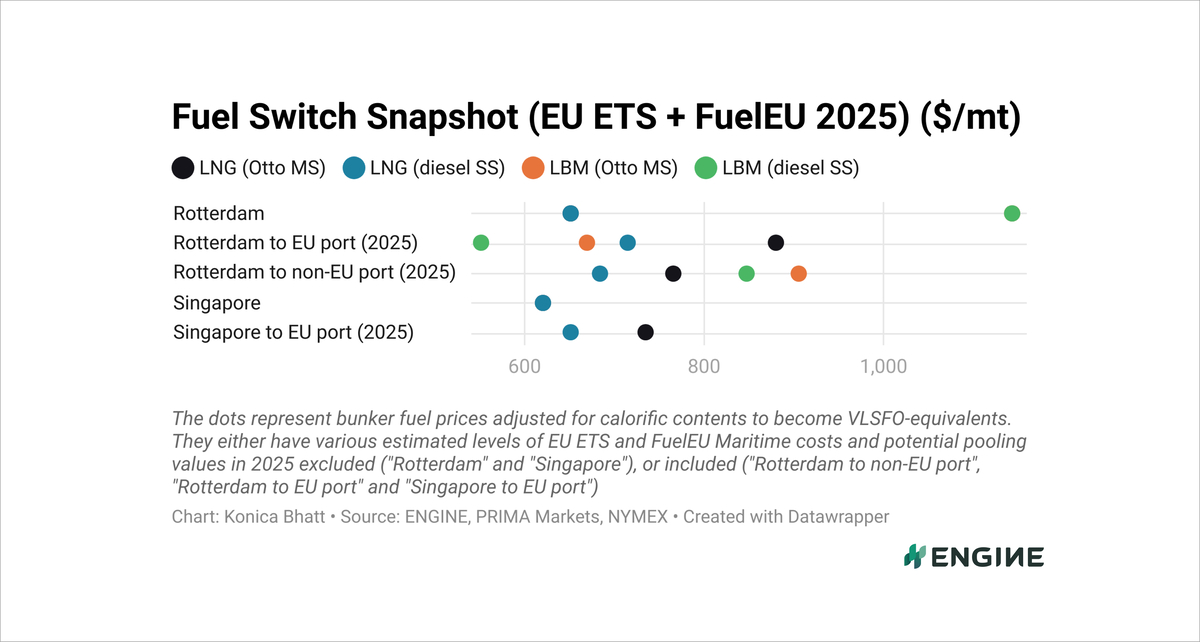

Rotterdam LNG up more than $60/mt in two weeks

All bunker prices mentioned below have been adjusted for calorific contents to make them VLSFO-equivalent. They have estimated EU-EU voyage compliance costs included for Rotterdam, and non-EU-EU compliance costs included for Singapore. These account for EU ETS costs and FuelEU Maritime penalties, and our estimated compliance surplus values for FuelEU pooling. Rotterdam's B100 and LBM prices also factor in Dutch HBE rebates for advanced liquid and gaseous biofuels sold in the Netherlands.

B100’s discount to VLSFO has widened to $170/mt in Rotterdam in the past week.

Using B100 instead of VLSFO now offers a theoretical FuelEU pooling benefit of $676/mt for a ship sailing between EU ports and selling on the compliance surplus it generates from using B100. This is down by $91/mt from the level seen on 9 May.

B100 is considered zero-carbon in the EU ETS which, combined with the theoretical pooling benefit and the Dutch HBE rebate, can reduce the real cost of bunkering B100 (HBE) to $610/mt.

B100 remains significantly more expensive in Singapore, carrying a $489/mt premium over VLSFO even after factoring in estimated pooling benefits for voyages between Singapore and an EU ports.

For dual-fuel vessels with Otto medium-speed (Otto MS) engines, LNG’s premium over VLSFO in Rotterdam has narrowed by $27/mt to $100/mt. In contrast, LNG now trades at a $65/mt discount to VLSFO when used in diesel slow-speed (diesel SS) engines.

Liquefied biomethane (LBM) is priced at a $162-210/mt discount to LNG in Rotterdam, depending on engine type.

Switching from LNG to LBM now offers a theoretical pooling benefit of $475–592/mt, up by $6–8/mt since 9 May. LBM remains the lowest-cost bunker fuel option for dual-fuel vessels in Rotterdam.

LBM's commercial attractiveness has not gone unnoticed. The fuel is now being tested and more regularly consumed by a range of container liners, car carriers and even some tankers buying on spot, three LBM bunker suppliers have told ENGINE in the past week.

Liquid fuels

The front-month ICE Brent Futures contract has surged $7.76/bbl ($57/mt) higher on an outright basis over the past week, driven up by Israel's war with Iran and mounting concerns over global oil supply disruptions.

Brent’s strong performance has lifted VLSFO prices in both Rotterdam and Singapore, which have increased by $57–62/mt over the past week.

Rotterdam’s B100 price has climbed $50/mt higher in the past week.

A source told ENGINE that the lead times for B100 deliveries in the Port of Amsterdam were estimated at 7–10 days last week, as barge bookings were filling up quickly.

Singapore’s B100 benchmark has increased $55/mt over the past week.

The port's B100 sales increased from 300 mt in April to 1,900 mt in May, according to preliminary data from the port authority.

Liquid gases

Rotterdam’s LNG price has spiked in yet another week, this time by $29/mt.

Singapore’s LNG bunker price has remained almost unchanged, edging higher by $3/mt.

Singapore’s LNG sales went up to 45,000 mt in May, a 3,000 mt rise from April. Some 1,450 mt/day of LNG was sold, up from 1,400 mt/day in April.

The port's total LNG bunker sales stood at 189,000 mt in the first five months of the year, up from 160,000 mt during the same period last year.

By Konica Bhatt

Please get in touch with comments or additional info to news@engine.online