Fuel Switch Snapshot: B100’s pooling value gains

B100 pooling value now estimated above $700/mt

B100-LBM spreads between $19-99/mt in Rotterdam

Singapore’s VLSFO-LNG spreads at $33-51/mt

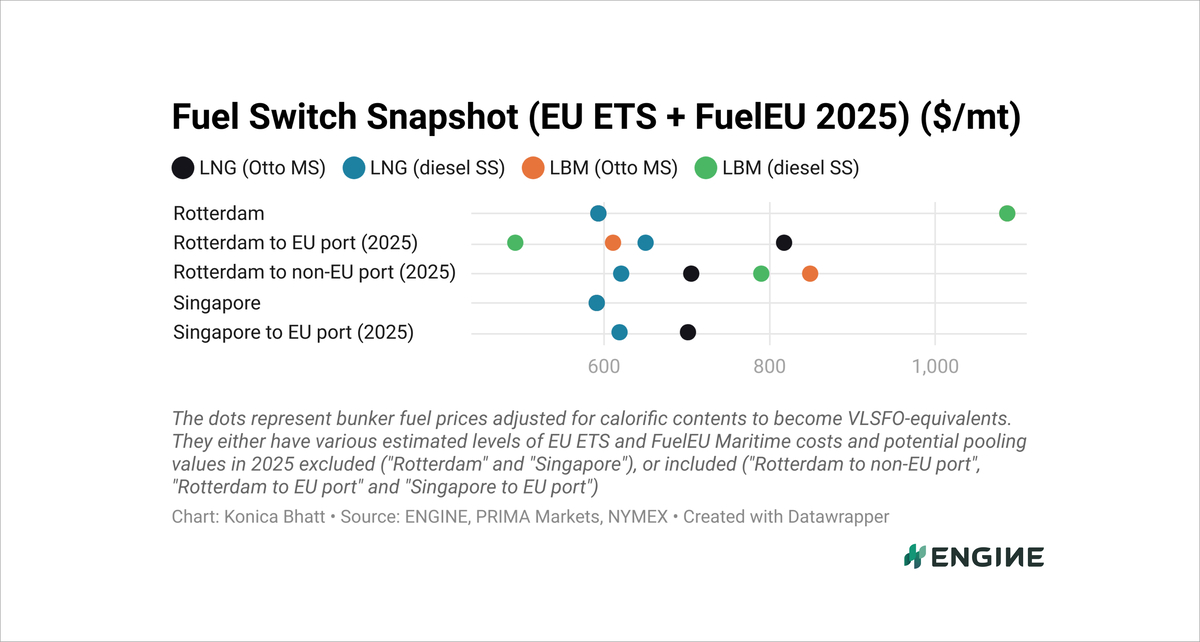

All bunker prices mentioned below have been adjusted for calorific contents to make them VLSFO-equivalent. They have estimated EU-EU voyage compliance costs included for Rotterdam, and non-EU-EU compliance costs included for Singapore. These account for EU ETS costs and FuelEU Maritime penalties, and our estimated compliance surplus values for FuelEU pooling. Rotterdam's B100 and LBM prices also factor in Dutch HBE rebates for advanced liquid and gaseous biofuels sold in the Netherlands.

All bunker prices mentioned below have been adjusted for calorific contents to make them VLSFO-equivalent. They have estimated EU-EU voyage compliance costs included for Rotterdam, and non-EU-EU compliance costs included for Singapore. These account for EU ETS costs and FuelEU Maritime penalties, and our estimated compliance surplus values for FuelEU pooling. Rotterdam's B100 and LBM prices also factor in Dutch HBE rebates for advanced liquid and gaseous biofuels sold in the Netherlands.

B100’s discount to VLSFO in Rotterdam has held steady at around $160/mt in the past week. That was only a marginal $2/mt increase from the week before. The theoretical FuelEU pooling benefit for vessels sailing between EU ports and selling surplus compliance from using B100 has risen by $25/mt to $716/mt.

Over in Singapore, B100 has narrowed its gap to VLSFO by $17/mt and now sits at a $446/mt premium after factoring in estimated regulatory benefits for Singapore-EU voyages.

B100 and liquefied biomethane (LBM) typically serve different vessel types, so a few will directly choose between the two. But for those looking to compare, Rotterdam's B100 is now $19/mt more expensive than LBM when used on vessels with Otto medium-speed (Otto MS) engines.

For diesel slow-speed (diesel SS) dual-fuel vessels, B100 is $99/mt more expensive than LBM, up $7/mt from the previous week.

Rotterdam’s fossil LNG is priced $102/mt below VLSFO for diesel SS engines, while Otto MS engines still face a $65/mt premium.

In Singapore, LNG’s premium over VLSFO has fallen to $51/mt for Otto MS engines and its discount has widened to $33/mt for diesel SS engines.

Liquid fuels

VLSFO prices in Rotterdam and Singapore have remained broadly steady in the past week. Rotterdam’s VLSFO benchmark has made a $6/mt decline, mostly tracking a $6/mt decline in the front-month ICE Brent Futures.

In contrast, Singapore’s VLSFO benchmark has inched up by $3/mt.

VLSFO delivery schedules in Singapore continue to vary significantly between suppliers. Some can deliver within five days, while others require advance bookings of up to three weeks. This represents a marginal improvement from last week's wide range of seven days to four weeks.

Rotterdam’s B100 price has declined by $9/mt over the past week, with downward pressure coming from a $9/mt increase in Prima Markets' assessed Dutch HBE rebate.

Bunker fuel supplier Burando Energies said it has delivered multiple B100 stems to Teekay Tankers vessels across the ARA region.

“The B100 supplied consisted entirely of residues originating from fatty acid methyl ester (FAME) production,” the company’s head of decarbonisation strategies, Nick de Haan told ENGINE. He advised lead times for this fuel at around 4-5 days.

Singapore’s B100 price has dropped by $14/mt over the past week.

Liquid gases

Rotterdam’s LNG price has fallen by $11/mt over the past week, while its LBM benchmark has dropped by $16/mt.

LNG is now priced $157–206/mt higher than LBM in Rotterdam, depending on a vessel’s engine type. VLSFO carries premiums of $141–259/mt over LBM in the port.

The theoretical FuelEU pooling benefit for vessels sailing between EU ports and selling surplus compliance from using Dutch-rebated LBM is estimated at $476-593/mt.

Singapore’s LNG bunker price has also edged down, declining by $4/mt over the past week.

By Konica Bhatt

Please get in touch with comments or additional info to news@engine.online