Fuel Switch Snapshot: Biomethane attractive with pooling

LBM by far the cheapest EU-EU compliance option

Rotterdam's B100–LSMGO spread holds above $400/mt

FuelEU pooling values dip on weaker euro exchange rate

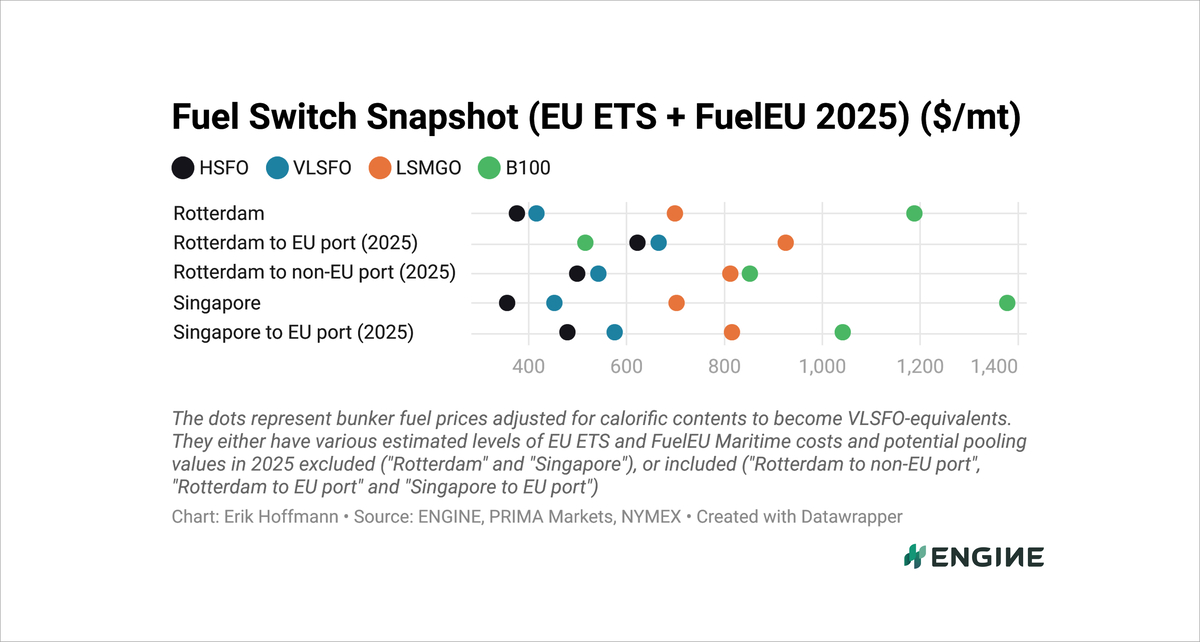

All bunker prices described in the text below have been adjusted for calorific contents to make them VLSFO-equivalent. They have estimated EU-EU voyage compliance costs included for Rotterdam, and nonEU-EU compliance costs included for Singapore. These account for EU ETS costs and FuelEU Maritime penalties, and the average price of compliance surpluses we have picked up from the FuelEU pooling market from the past week. Rotterdam's B100 and LBM prices also factor in Dutch HBE rebates for advanced liquid and gaseous biofuels sold in the Netherlands.

All bunker prices described in the text below have been adjusted for calorific contents to make them VLSFO-equivalent. They have estimated EU-EU voyage compliance costs included for Rotterdam, and nonEU-EU compliance costs included for Singapore. These account for EU ETS costs and FuelEU Maritime penalties, and the average price of compliance surpluses we have picked up from the FuelEU pooling market from the past week. Rotterdam's B100 and LBM prices also factor in Dutch HBE rebates for advanced liquid and gaseous biofuels sold in the Netherlands.

Rotterdam’s HBE-rebated liquefied biomethane (LBM) with 0gCO2e/MJ is at a massive $397/mt discount to fossil LNG. The discount was even greater last week, and has since narrowed by $27/mt.

LBM is also at large discounts to B100 in Rotterdam. When the LBM is consumed in an Otto medium speed (Otto MS) engine it costs $211/mt less than B100, and $370/mt less when it powers a diesel slow speed (diesel SS) engine.

Rotterdam’s fossil LNG outcompetes LSMGO by $222/mt when it is consumed in Otto MS engines, and by $382/mt in diesel SS engines.

Singapore’s fossil LNG can also make sense in some cases for voyages to the EU. If the LNG powers a diesel SS engine, it is $7/mt cheaper than VLSFO, but in an Otto MS engine it is $73/mt more expensive.

Rotterdam’s HBE-rebated B100 looks attractive for vessels running on liquid fuels between EU ports. It is at discounts of $105/mt to HSFO, $148/mt to VLSFO and $409/mt to LSMGO.

Most of Europe is now covered by 0.10% sulphur Emission Control Areas (ECAs). B100 is virtually sulphur-free and competes with LSMGO - or HSFO with scrubbers – for most EU-EU legs.

A $409/mt B100 discount to LSMGO is huge and made possible through FuelEU Maritime pooling. B100 that meets RED II/III requirements has a zero-emission factor towards the EU ETS, and can generate a FuelEU compliance surplus of around €190-230/mtCO2-equivalent ($519-716/mt). A company can then either transfer this surplus to non-compliant vessels in its own fleet or sell it to another company in a pool.

Singapore’s B100 is not competitive with HSFO, VLSFO or even LSMGO on voyages to the EU. B100 is hardly bunkered in Singapore. Just 21,000 mt has been sold this year, compared to 853,000 mt bio-VLSFO and 342,000 mt bio-HSFO, according to the port’s official numbers.

Neither is Singapore’s B30-VLSFO price, which is at a $113/mt premium over pure VLSFO on voyages from Singapore to EU ports.

Liquid fuels

Regulation-adjusted B100 prices have come down by $16/mt in Rotterdam and $17/mt in Singapore in the past week.

Rotterdam’s B100 price has fallen along with the price of POMEME – a key biofuel type. Prima Markets’ non-HBE-rebated POMEME CIF ARA barge price has dropped by $32/mt on the week to $1,585/mt.

A $7/mt weekly drop in our assessed FuelEU Maritime pooling value for B100 consumed on EU-EU voyages has weakened B100’s competitiveness slightly, but not enough to offset the overall price drop. The average of seven compliance surplus levels gathered in the past week was around €216/mtCO2e/MJ ($670/mt of B100).

Singapore’s UCOME-based B100 price has shed some value despite a steady UCOME FOB China barge price assessed by Prima to $1,180/mt this week.

The potential pooling value for Singapore’s B100 for nonEU-EU voyages has dropped by $3/mt on the week to $335/mt.

Liquid gases

Rotterdam’s fossil LNG bunker price has come off amid shrinking bunker delivery premiums and a TTF gas futures dip. Front-month TTF has traded down as market participants speculate about a breakthrough in Russia-Ukraine peace talks.

Rotterdam’s LBM has shed $11-13/mt in the past week amid $9-11/mt falls in the assessed pooling values of LBM sold with 0gCO2e/MJ. The pooling value for this LBM consumed in Otto MS engines has dropped to $930/mt, and to $1,090/mt for diesel SS engines. The weekly change in the pooling value is mostly down to a weaker euro-dollar exchange rate.

Singapore’s LNG bunker price has edged up and flipped from a discount to a premium over Rotterdam’s falling price. The port’s bunker delivery premium is roughly steady at $1.83/MMBtu (95/mt), while the front-month NYMEX Japan/Korea Marker (JKM) increased by $0.34/MMBtu to $11.47/MMBtu ($596/mt).

“North Asia LNG prices in the spot market jumped to a two-month high, aided by a surge in spot freight rates,” ANZ Bank’s Daniel Hynes commented.

By Erik Hoffmann

Please get in touch with comments or additional info to news@engine.online