Fuel Switch Snapshot: EU regs boost B100 and LBM

B100 premium over VLSFO shoots up

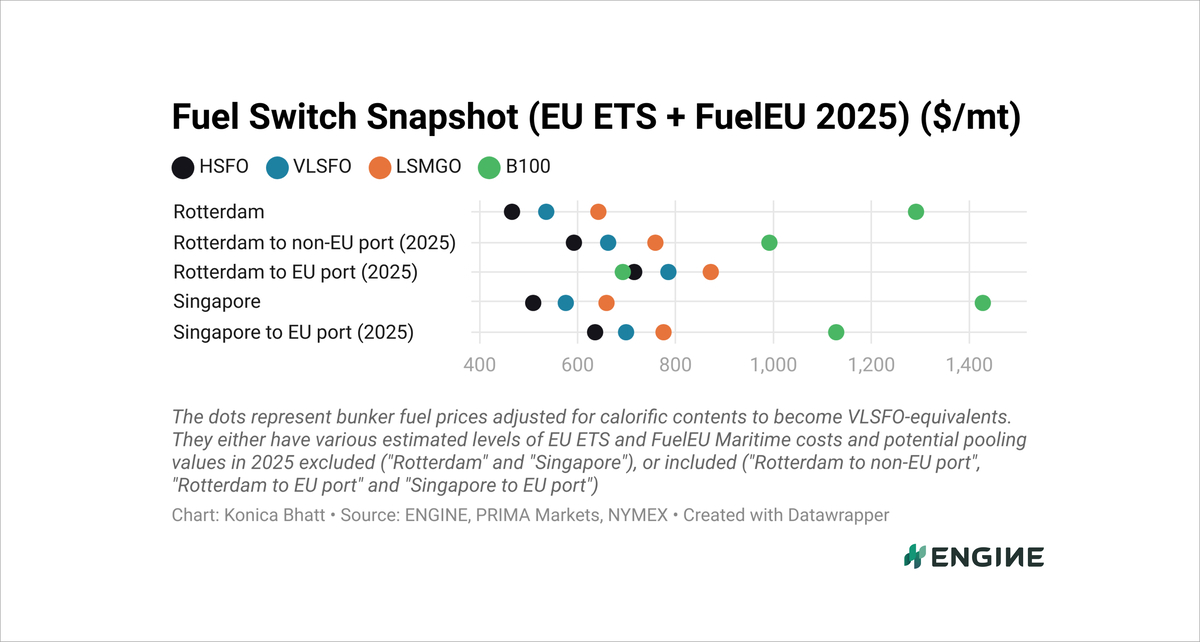

B100 and LBM cheaper than HSFO with EU costs

When factoring in the EU ETS compliance costs and FuelEU pooling benefits for voyages between two EU ports, the VLSFO-equivalent price of B100 (100% biofuel) remains lower than the VLSFO-equivalent price of HSFO in Rotterdam.

This is because using B100 instead of VLSFO on ships offers a theoretical pooling benefit of $600/mt under FuelEU. This potential pooling benefit has gained $59/mt in the past week. Since B100 is considered zero-carbon under the EU ETS, the combined effect of compliance savings and the pooling benefit can reduce B100’s real bunkering cost to $691/mt.

In comparison, HSFO’s real bunkering cost will rise to $715/mt when factoring in FuelEU and EU ETS compliance penalties for a vessel travelling between two EU ports.

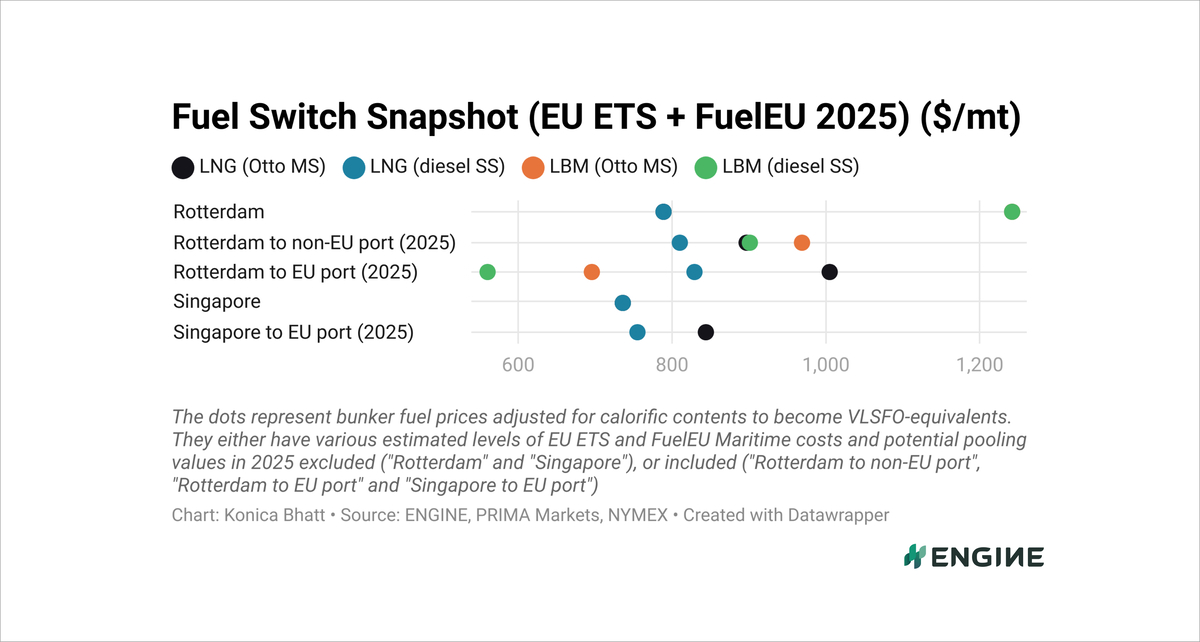

LBM has also become cheaper than HSFO with EU compliance for voyages between two EU ports. When used in an Otto medium-speed engine with a 3.1% methane slip, it offers a theoretical pooling benefit of $546/mt. Combined with EU ETS compliance savings, this reduces the real bunkering cost of LBM to $696/mt.

The pooling benefit increases further to $681/mt when LBM is used in a diesel slow-speed (SS) marine engine with a minimal methane slip of 0.2%, reducing the real bunkering cost to $561/mt.

Liquid fuels

Rotterdam's VLSFO-equivalent B100 price has surged by $73/mt over the past week, increasing its compliance premium over VLSFO to $643/mt.

Singapore's bio-blended bunker sales rose by 1% in January, after two consecutive months of decline. Total sales reached 108,000 mt, up from 106,000 mt in December.

Rotterdam’s VLSFO price has remained relatively stable, declining by just $6/mt over the past week. In contrast, Singapore’s VLSFO benchmark has posted a modest $7/mt gain over the same period.

Liquid gases

Rotterdam’s VLSFO-equivalent LNG price has declined by $26/mt over the past week, after recording three straight weeks of gains. This drop is linked to an almost 4% decrease in the front-month Dutch TTF Natural Gas contract.

Upcoming talks between the US and Russia aimed at ending the Russia-Ukraine war appear to have weighed on market sentiment, pushing the TTF benchmark lower.

Singapore’s VLSFO-equivalent LNG benchmark has remained relatively stable, rising by just $10/mt over the past week. Meanwhile, the port’s LNG bunker sales have plummeted by 86% over the past month, dropping to just 200 mt/day in January, from 1,600 mt/day in December.

By Konica Bhatt

Please get in touch with comments or additional info to news@engine.online