Fuel Switch Snapshot: FuelEU pooling values slide

ENGINE’s FuelEU pooling values for B100, LBM drop

Singapore’s B100 gains nearly $30/mt

LNG $60-168/mt costlier than B100 in Rotterdam

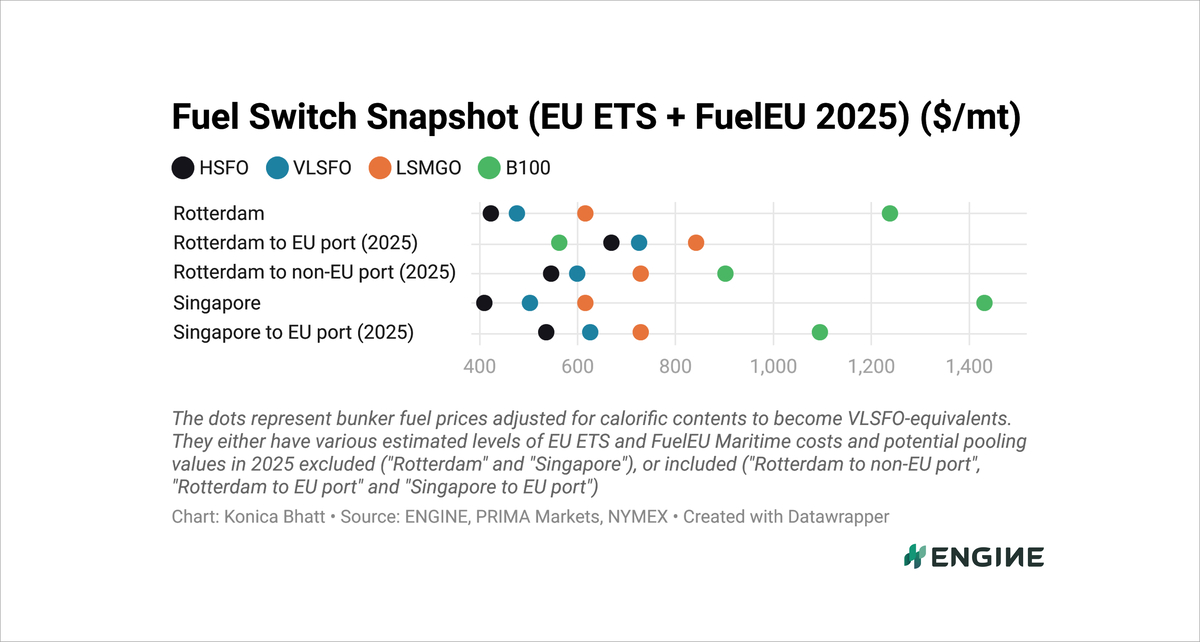

All bunker prices mentioned below have been adjusted for calorific contents to make them VLSFO-equivalent. They have estimated EU-EU voyage compliance costs included for Rotterdam, and non-EU-EU compliance costs included for Singapore. These account for EU ETS costs and FuelEU Maritime penalties, and our estimated compliance surplus values for FuelEU pooling. Rotterdam's B100 and LBM prices also factor in Dutch HBE rebates for advanced liquid and gaseous biofuels sold in the Netherlands.

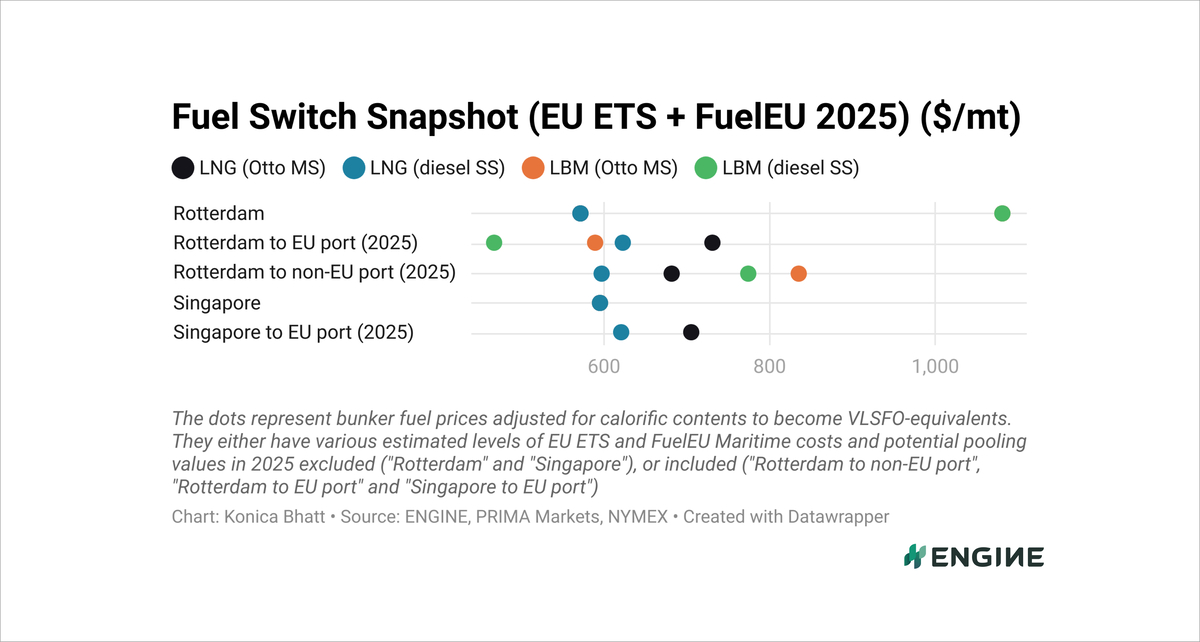

All bunker prices mentioned below have been adjusted for calorific contents to make them VLSFO-equivalent. They have estimated EU-EU voyage compliance costs included for Rotterdam, and non-EU-EU compliance costs included for Singapore. These account for EU ETS costs and FuelEU Maritime penalties, and our estimated compliance surplus values for FuelEU pooling. Rotterdam's B100 and LBM prices also factor in Dutch HBE rebates for advanced liquid and gaseous biofuels sold in the Netherlands.

ENGINE-assessed FuelEU pooling benefits have fallen across both B100 and liquefied biomethane (LBM) over the past week.

The theoretical pooling benefit for vessels sailing between EU ports and selling compliance surpluses from Dutch-rebated B100 has dropped by $72/mt to an estimated $676/mt.

For dual-fuel ships equipped with Otto medium-speed engines in Rotterdam, LBM’s pooling value has declined by $13/mt to $492/mt.

Vessels equipped with diesel slow-speed (diesel SS) engines and minimal methane slip of about 0.2% can generate an estimated pooling benefit of roughly $613/mt, marking a $17/mt decline from the previous week.

Rotterdam's LBM consumed in diesel SS engines is still the most cost-effective option for EU-EU voyages. It is priced $94/mt lower than B100, even if its discount to B100 has narrowed by $5/mt in the past week.

Rotterdam’s LNG is now at $60-168/mt premiums over B100, and $141-155/mt premiums over LBM. The premiums depend on the engine type.

Liquid fuels

Rotterdam’s VLSFO price has been steady, edging up by just $2/mt in the past week.

VLSFO, HSFO and LSMGO supply remains stable in the ARA bunkering hub, but stems should be booked around 5-7 days ahead as availability is tighter for prompt delivery with several suppliers, a trader told ENGINE.

Singapore’s VLSFO has dropped by $8/mt in the past week. VLSFO availability in the port has improved, with most suppliers now recommending lead times of 4–11 days, compared to last week’s wide range of up to three weeks. However, a source noted that supply could tighten again in the coming days amid strong demand.

Rotterdam’s B100 benchmark has also remained almost steady with a $2/mt weekly decline. On the other hand, Singapore's B100 price has gained $27/mt in the past week.

Liquid gases

Rotterdam’s LNG bunker price has fallen for the second consecutive week, largely due to a 2% decline in the front-month Dutch TTF Natural Gas contract, a key benchmark for European gas prices.

“Expectations of easing tensions due to ceasefire negotiations between the US and Russia, as well as forecasts of an easing of the heat wave in Europe,” have weighed on TTF prices, according to the Japan Organization for Metals and Energy Security (JOGMEC).

Singapore’s LNG bunker price has held steady from the previous week, reflecting stability in the front-month NYMEX Japan/Korea Marker (JKM), which typically guides Asian LNG bunker prices.

By Konica Bhatt

Please get in touch with comments or additional info to news@engine.online