Fuel Switch Snapshot: Green gas gets lots of points

Two weeks into 2025, we note that sustainable biofuels make sense as a cost-effective way for most EU-trading vessels to comply with FuelEU Maritime, and to lower their exposure to EU Emissions Trading System (EU ETS) costs.

And we introduce liquefied biomethane (LBM), a renewable gas with similar characteristics as liquefied natural gas (LNG). On the face of it, it looks exorbitantly expensive, but with FuelEU pooling the picture changes completely.

Liquid gases

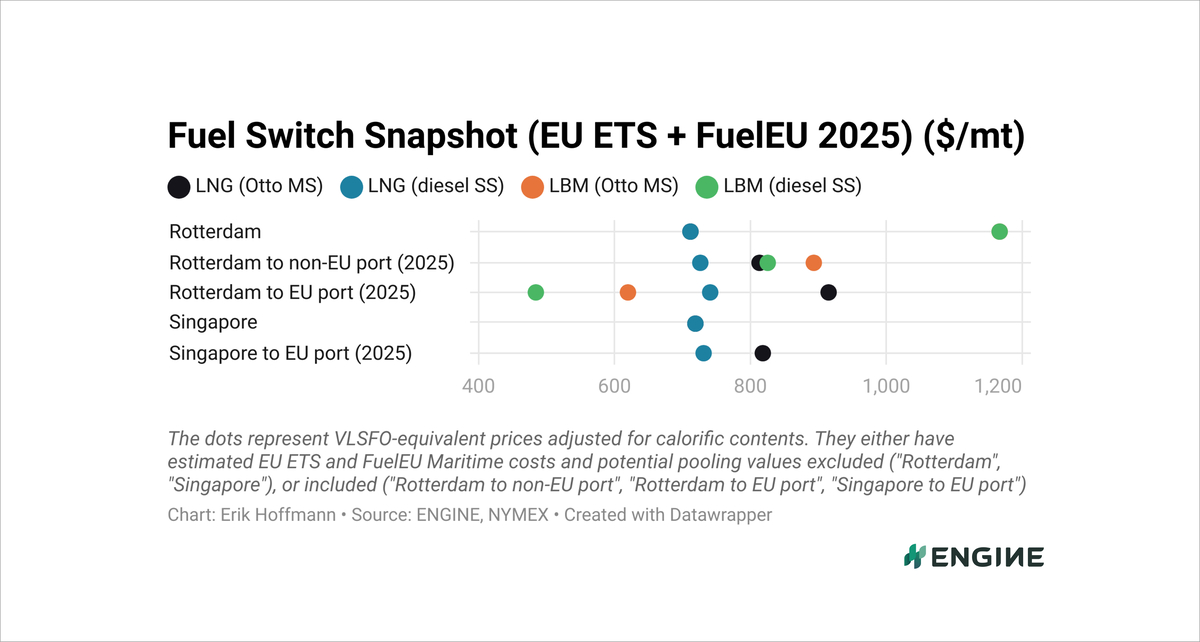

LBM is pricy in Rotterdam, even with a €40/MWh ($628/mt) Dutch rebate included. It comes in at nearly $1,200/mt on a VLSFO-equivalent basis. This is without the dual impacts of the EU ETS and FuelEU regulations added as costs to the price.

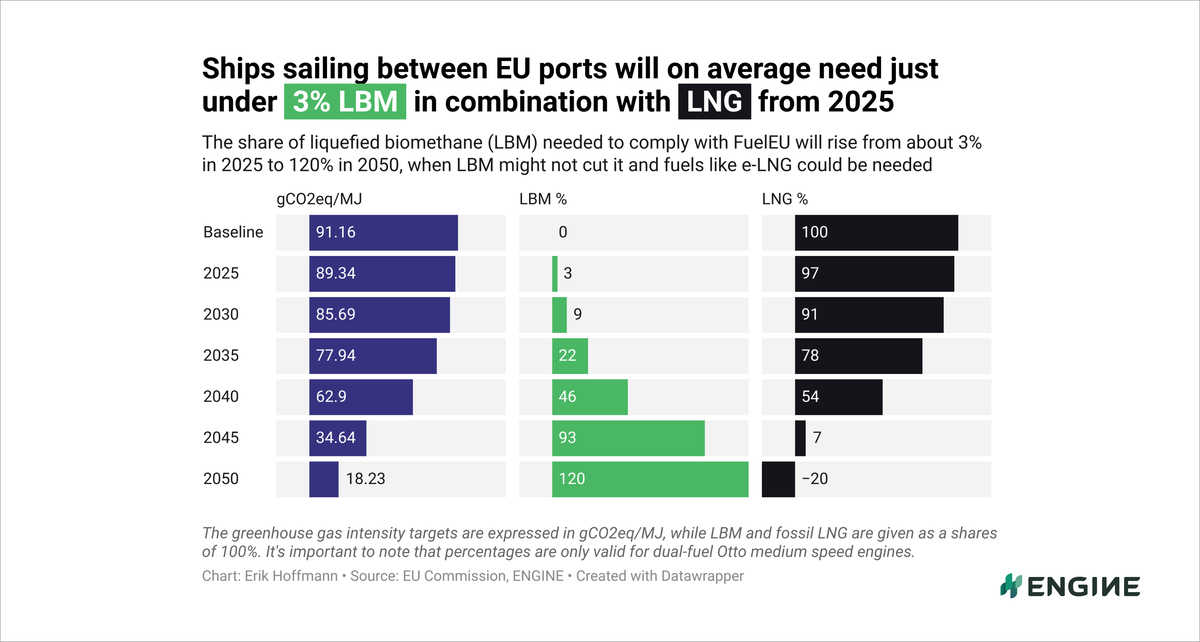

It gets much more interesting with the FuelEU pooling mechanism. LBM has a significantly lower GHG intensity than fossil LNG. It’s overcompliant with the 2% GHG reduction target for 2025 and will generate considerable compliance surpluses when it is consumed in both Otto medium speed engines (Otto MS) with high methane slips, and in diesel slow speed engines (diesel SS) with low methane slips.

Methane slip is a key part of the calculation as methane has 28 times higher global warming potential than carbon dioxide (CO2) and is penalised by the EU accordingly. An LNG-fuelled ship with an Otto MS engine has a methane slip of 3.1% and will actually be undercompliant with FuelEU from year one. This is where LBM comes in, as this renewable gas can be physically blended or mass-balanced with LNG without compatibility issues on consuming ships.

LBM consumed in a low methane slip engine between two EU ports could actually become the cheapest gas compliance option. Despite commanding a premium of about $550/mt on top of fossil LNG in Rotterdam, LBM can benefit from a pooling mechanism in FuelEU that allows transfer of compliance surpluses across vessels in a fleet, or between fleets when they are pooled together.

A ship with an Otto MS engine running on LBM will generate enough compliance surpluses to cover around 36 ships of the same kind running on fossil LNG with the same fuel consumption over the same distance.

For LBM-fuelled ships with diesel SS engines that figure is greater still. Just one of these ships can cover the compliance of 45 ships with Otto MS engines fuelled with fossil LNG.

Even Otto MS engines (highest methane slip) can consume LBM at a lower estimated overall cost than fossil LNG-fuelled diesel SS engines (lowest slip).

Liquid fuels

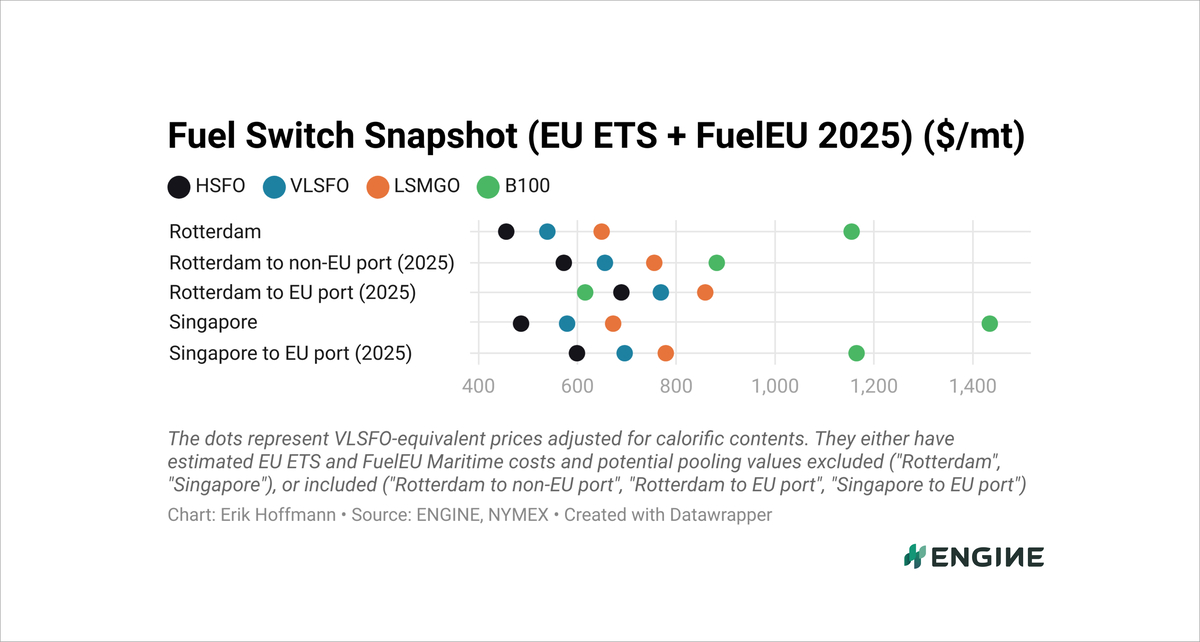

A vessel taking 100% biofuel (B100) in Rotterdam can enjoy a rebate of over $300/mt through the Dutch HBE system. If that vessel consumes the B100 in a 0.10% sulphur-capped Emission Control Area (ECA), the B100 will outcompete LSMGO on overall costs as long as the overcompliance generated by that B100-consuming ship is transferred or sold at a value equal to or higher than the cheapest FuelEU compliance option.

B100 is far from attractive on an outright price basis, but with estimated EU ETS and FuelEU costs for all fuels added, and with Dutch HBE rebates subtracted, B100 starts to make sense in Rotterdam. It’s even cheaper than HSFO when we include EU compliance costs for voyages between two EU ports.

All the prices here have been converted to VLSFO-equivalents, which means they have the same energy content per mt of fuel and can be compared head-to-head with one another.

B100 is priced considerably lower in Rotterdam than in Singapore. That’s because it’s rebated in the Dutch HBE incentive system for renewable fuels, whereas Singapore has no such rebates. B100 is also a much more common grade for bunker suppliers to carry in the ARA, as there are no restrictions on how much biofuel they can carry as a share of a batch of fuel. In Singapore and most other ports, it’s capped at 25% biofuel.

EUAs

Estimated EU Allowance (EUA) costs are slightly down on the week, from $170/mt to $167/mt for VLSFO and HSFO this year, and from $175/mt to $172/mt for LSMGO between two EU ports.

These costs are with 70% of the EU ETS phased in for this year, and only cover tank-to-wake CO2 emissions. LNG has lower CO2 emissions than the conventional fuels and costs shipowners about $150/mt to burn with current EUA prices.

By Erik Hoffmann

Please get in touch with comments or additional info to news@engine.online