Fuel Switch Snapshot: Hormuz closure sends bunker prices soaring in major ports

Hormuz disruption sends ripples through B100, LBM prices

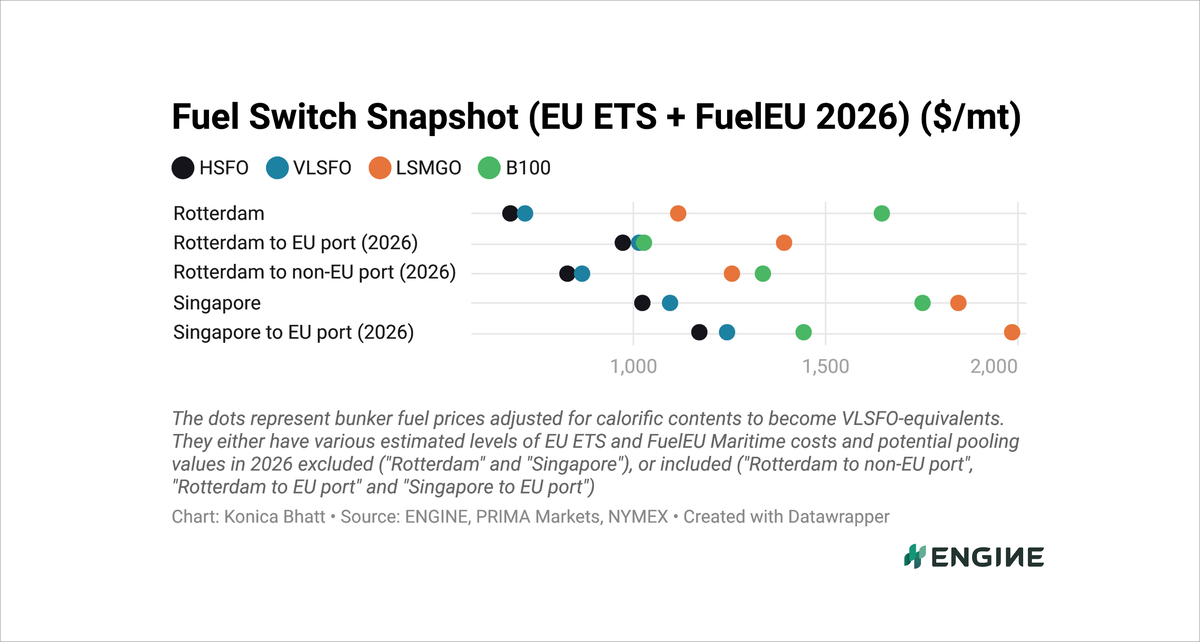

Rotterdam’s B100 shifts to premium over VLSFO

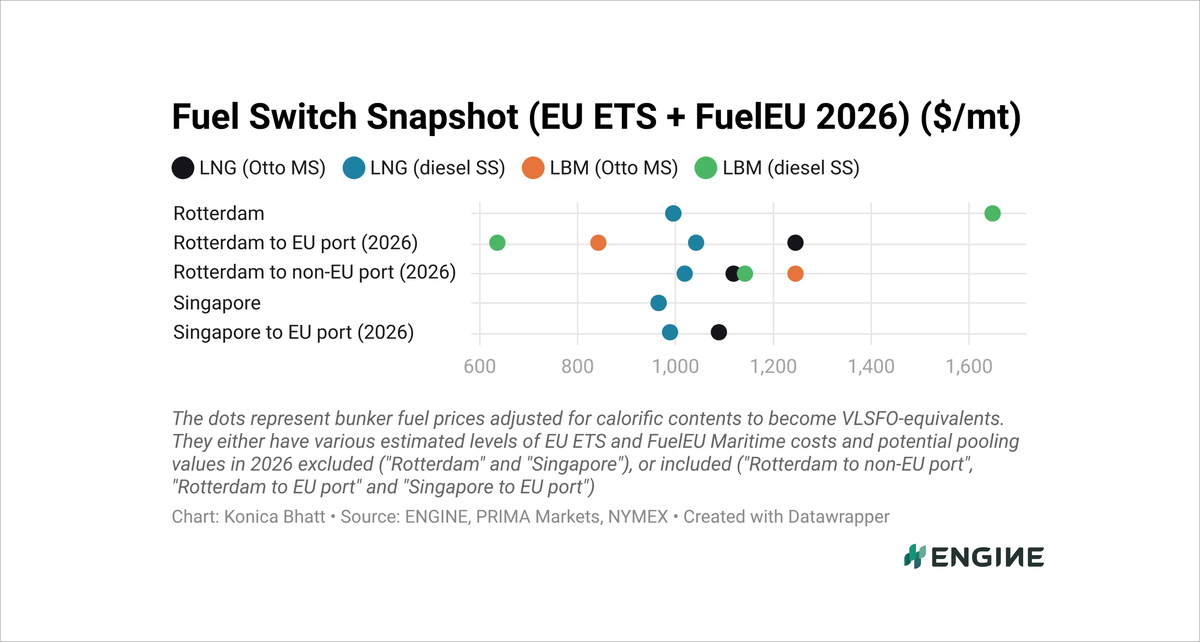

LNG at heavy discounts to LSMGO in Singapore

The closure of the Strait of Hormuz amid the escalating Middle East conflict and supply disruptions across the region has pushed conventional and gas bunker fuel prices sharply higher over the past week.

Singapore's and Rotterdam’s HSFO and VLSFO prices have tracked a drastic surge in the front-month ICE Brent contract (+$173/mt) and LSMGO prices have climbed even higher on a jump in low-sulphur gasoil futures (+$479/mt).

The shock has rippled across alternative fuels as well.

Biofuels and liquefied biomethane (LBM) prices have also surged, with the EU compliance costs further reshaping bunker economics in major ports.

Rotterdam’s B100 has flipped to a $14/mt premium over VLSFO from a $289/mt discount, and to a $53/mt premium over HSFO from a $239/mt discount in the past week.

B100’s discounts to LNG in Rotterdam have narrowed by $178–195/mt to $17–217/mt, depending on the vessel’s engine type.

LNG has also reversed course. The fuel has flipped to a $31/mt premium over VLSFO from a $94/mt discount when bunkered in diesel slow-speed engines with low methane slip.

At the same time, its discount over LSMGO has widened by $54/mt to $350/mt for diesel slow-speed engines.

Liquid fuels

Rotterdam’s B100 price has spiked by $501/mt, massively exceeding an $82/mt weekly rise in the Prima Markets-assessed ARA POMEME barge price.

Biofuel bunker prices did not respond as rapidly to the oil price shock at the start of last week as VLSFO and LSMGO prices did. That created pricing opportunities for B100 and B30-LSMGO against pure LSMGO for EU-EU voyages. B100 and B30-LSMGO’s discounts to LSMGO widened initially.

Later in the week, biofuel prices caught up as biofuel bunker suppliers priced closer to what they could get for their fuel rather than where underlying POMEME wholesale prices were at.

ENGINE then saw a sharp rise in B100 price indications from certain suppliers on Monday, which contributed to make B100 more expensive than HSFO and VLSFO on EU-EU voyages for the first time since FuelEU Maritime came into effect. It should be noted that VLSFO can’t be used on many EU-EU voyages as most of these will be in 0.10% sulphur-capped Emission Control Areas (ECAs). And HSFO can’t be used in these areas without scrubbers.

Potential FuelEU Maritime pooling values have dropped to make the value of B100’s compliance surplus less worth. OceanScore’s FuelEU pooling index fell by €19/mtCO2e over the past week, cutting B100’s potential pooling value by $70/mt to $624/mt.

Singapore’s B100 price has surged $291/mt higher. In addition to strong upward pressure from the oil price rally, some upward pressure has come from rising UCOME wholesale costs. Prima Markets assessed its China UCOME cargo benchmark up by $40/mt on the week.

Liquid gases

IMF Portwatch data shows that just one tanker passed through the Strait of Hormuz on 5 March, down from 11 on 1 March and much below the peak of 73 recorded on 22 February. And gas bunker markets have reacted sharply to the disruption as well.

Rotterdam’s LNG bunker prices have surged $306–322/mt over the past week, while LBM prices have climbed even more steeply by $448–464/mt.

LNG’s premiums over LBM in Rotterdam have narrowed by $142/mt each to $401–407/mt, depending on the engine type.

Singapore’s LNG bunker prices have gained $372–380/mt.

LNG’s discounts to LSMGO have widened significantly in both Rotterdam and Singapore.

Rotterdam’s LNG has become more affordable against its LSMGO, with the spread widening by $54–70/mt to $149–350/mt over the past week.

In Singapore, LNG’s discounts to LSMGO have widened by a striking $750–758/mt to $894–995/mt, depending on the engine type.

"With Qatari LNG production curbed and Iranian attacks on major infrastructure, Asian buyers scrambled to replace cargoes, pushing prices to new highs," Andy Soomer, bunker supplier Axpo Group's head of fundamental analysis said.

"A prolonged interruption will likely drive prices higher to trigger demand destruction and ensure European gas inventories are refilled," Soomer added.

By Konica Bhatt

Please get in touch with comments or additional info to news@engine.online