Fuel Switch Snapshot: LNG costlier than VLSFO

Singapore’s VLSFO price is cheaper than LNG

LNG approaches parity with VLSFO in Rotterdam

Price gap between biofuel and LNG shrinks

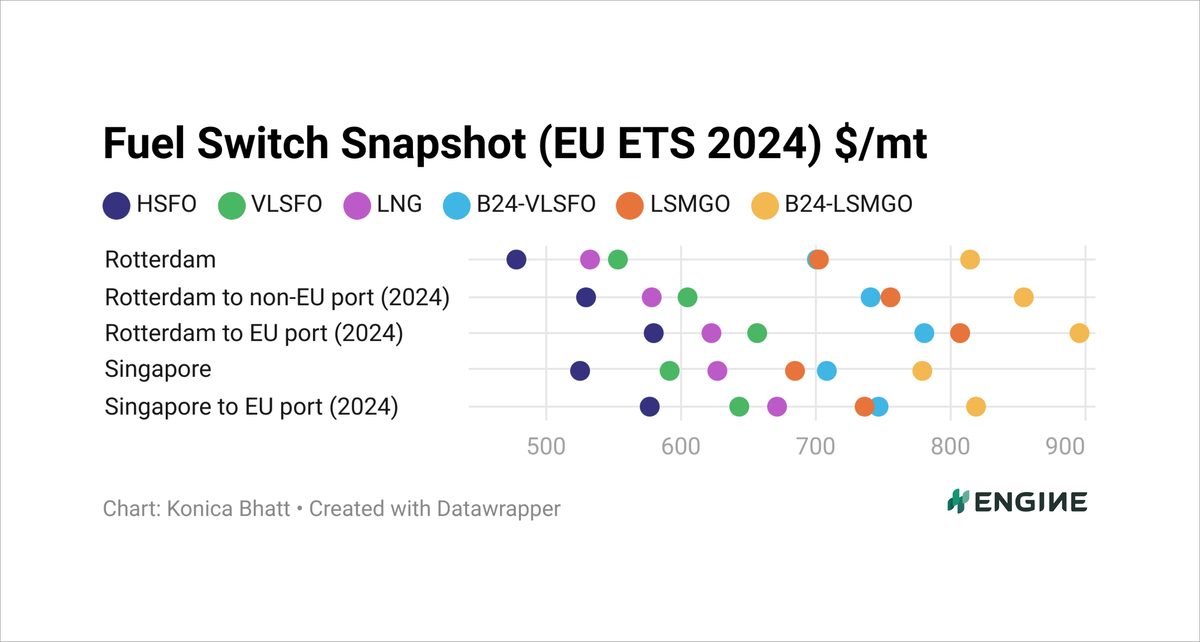

CHART: The dots represent bunker fuel prices adjusted for calorific contents to become VLSFO-equivalents, and with various estimated levels of EU ETS costs excluded (Rotterdam) and included (Rotterdam to non-EU port and Rotterdam to EU port). ENGINE, PRIMA Markets, NYMEX

CHART: The dots represent bunker fuel prices adjusted for calorific contents to become VLSFO-equivalents, and with various estimated levels of EU ETS costs excluded (Rotterdam) and included (Rotterdam to non-EU port and Rotterdam to EU port). ENGINE, PRIMA Markets, NYMEX

LNG bunker benchmarks in Rotterdam and Singapore continue to rise sharply.

With estimated EU Allowance (EUA) costs included in bunker fuel costs, Singapore's LNG bunker price has surged $34-37/mt in the past week after a $29-30/mt jump the week prior.

After adjusting the price for calorific contents to become VLSFO-equivalent, Singapore's LNG price has flipped to a premium of $29-36/mt over its VLSFO in the past week, from a $30-36 discount noted a week prior.

Rotterdam's fossil LNG bunker price has closed even further on VLSFO by $33-34/mt over the past week, making it only $20-33/mt cheaper than VLSFO now.

Biofuel price premium in Singapore over fossil LNG has dropped by another $61-62/mt to $75-81/mt in the past week. In Rotterdam, the bio-bunker premium over LNG has narrowed by $11/mt to $156-168/mt.

VLSFO

Rotterdam's VLSFO price has mostly followed Brent's downward movement over the past week. Rotterdam’s VLSFO benchmark has declined by $11-18/mt in the past week, depending on whether the estimated EUA costs are included.

Availability of VLSFO is normal in Rotterdam, with lead times of 3-5 days recommended to ensure full coverage from suppliers, a trader said.

Singapore’s VLSFO benchmark has also tracked Brent’s movement, falling $32/mt over the past week.

Lead times for VLSFO in Singapore have exhibited significant fluctuations recently. Most suppliers now recommend lead times of up to 10 days for this grade, while some can accommodate stems within five days.

Biofuels

Rotterdam’s B24-VLSFO HBE bunker price has inched $5/mt higher in the past week. When we add estimated EUA costs, the price has gained $8-10/mt, depending on whether we are looking at voyages between EU ports or between EU ports and non-EU ports.

A huge gain in the price of palm oil mill effluent methyl ester (POMEME) feedstock – qualified for Dutch HBE rebates – has pushed the price higher. PRIMA-assessed POMEME price in the ARA has jumped by $70/mt to $1,368/mt in the past week.

In contrast, Singapore’s B24-VLSFO UCOME bunker price has slumped by $25-28/mt, depending on whether the price is adjusted with estimated EUA costs.

The price has declined amid a $10/mt drop in UCOME FOB China, according to PRIMA Markets. Chinese biodiesel exports to the EU are being investigated by the European Commission for "unfairly traded biodiesel". The ongoing investigation has dented Chinese biodiesel inflows into European countries.

LNG

Rotterdam and Singapore’s LNG bunker prices have seen significant upticks in the past week.

Rotterdam’s LNG bunker benchmark has climbed $16-22/mt higher, depending on whether estimated EU ETS costs are included in the cost of fuel. This increase has been driven by the underlying front-month NYMEX Dutch TTF Natural Gas benchmark, which has seen an uptick due to heavy maintenance activities at Norwegian gas facilities.

Singapore’s LNG bunker benchmark has risen by a staggering $34-37/mt in the past week. The movement is influenced by the upward trend in the underlying Japan/Korea Marker (JKM) gas benchmark and prevailing trends in the Asian LNG market.

Analysts at ANZ Bank noted that “the rally in global gas prices continued amid ongoing buying from importers.” Importers such as Japan and South Korea are restocking gas inventories ahead of the Northern Hemisphere summer, further driving demand.

By Konica Bhatt

Please get in touch with comments or additional info to news@engine.online