Fuel Switch Snapshot: LNG still an expensive choice for dual-fuel vessels

LNG not competitive with VLSFO since July

LSMGO still a cost-effective option in ECAs

Advanced Dutch biofuel prices up amid lower rebate

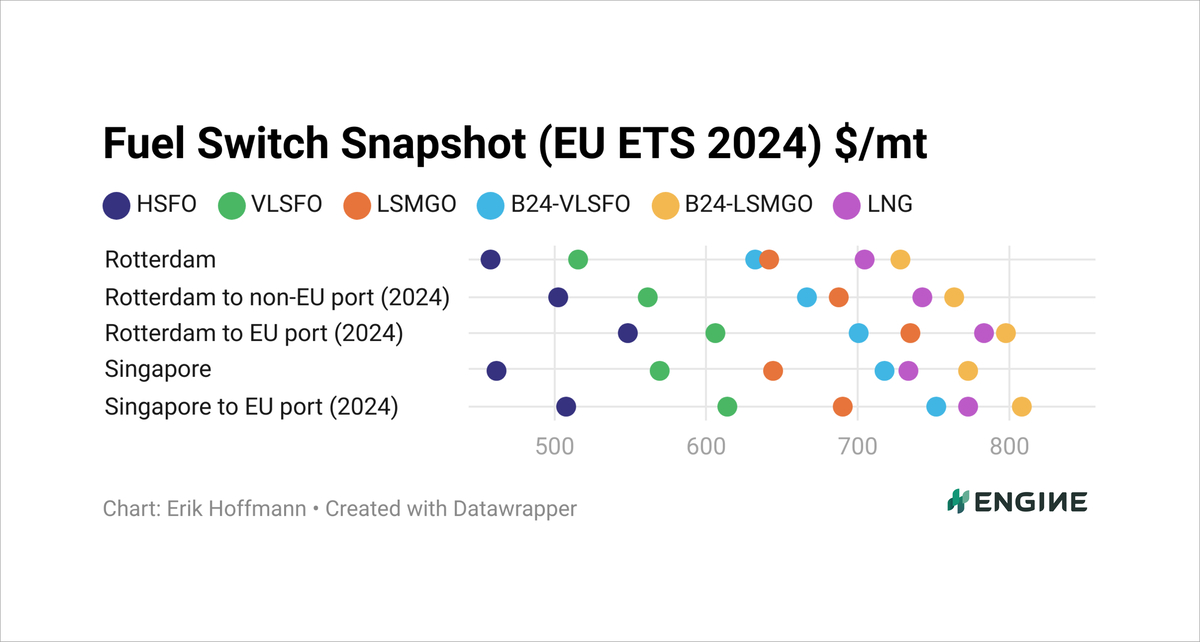

CHART: The dots represent bunker fuel prices adjusted for calorific contents to become VLSFO-equivalents, and with various estimated levels of EU ETS costs in 2024 excluded (Rotterdam) and included (Rotterdam to non-EU port and Rotterdam to EU port). ENGINE, PRIMA Markets, NYMEX

CHART: The dots represent bunker fuel prices adjusted for calorific contents to become VLSFO-equivalents, and with various estimated levels of EU ETS costs in 2024 excluded (Rotterdam) and included (Rotterdam to non-EU port and Rotterdam to EU port). ENGINE, PRIMA Markets, NYMEX

For dual-fuel LNG-capable vessels without scrubbers sailing outside of 0.10% sulphur-capped Emission Control Areas (ECAs), VLSFO grade has been a more cost-effective choice than LNG in Rotterdam for four months now. For vessels of this kind sailing within ECAs, LSMGO has often been a more attractively priced option than LNG over the past three months, but it has been on and off.

This is when we compare the grades as VLSFO-equivalents on energy content, which is what matters for how far a vessel can sail on a quantity of fuel.

Rotterdam’s VLSFO-equivalent LNG was last at a discount to VLSFO in late July, and has since pulled ahead to wide premiums. LNG was competitive with LSMGO (both as VLSFO-equivalents) in early November and has since shot up to premiums.

Rotterdam’s LNG price has been rather steady in the past week, while VLSFO and LSMGO have made more marked gains. VLSFO-equivalent LNG now stands at $694/mt, a massive $178/mt premium above VLSFO and also $51/mt above LSMGO.

LNG’s premium over LSMGO is slightly narrower at $45/mt with estimated EU Allowance (EUA) costs added – which favours LNG’s lower CO2 emissions – for voyages between EU ports and non-EU ports. Voyages between two ports require more EUAs to be surrendered, and with the estimated costs of those extra EUAs added LNG’s premium over LSMGO drops to $38/mt.

VLSFO

Front-month ICE Brent rallied 6% higher last week on continuous support from the ever-escalating Russia-Ukraine war. On Thursday last week, Russian President Vladimir Putin announced that Russia had fired a ballistic missile at Ukraine and warned of a potential global nuclear war, increasing fears of oil supply disruptions, Reuters reported.

Despite this $4.13/bbl ($30/mt) Brent gain, VLSFO prices only creeped up by $4/mt in Rotterdam and $9/mt in Singapore. The ports’ LSMGO levels made bigger $20-22/mt gains, but still underperformed against Brent.

A slight improvement in VLSFO supply in the ARA might have contributed to put a lid on prices, but lead times are still relatively long at 5-7 days for the grade. LSMGO availability is relatively better in the ARA hub and most suppliers can offer the grade for prompt delivery dates. Lead times of around 3-5 days are advised.

VLSFO availability tightened in Singapore, with lead times at 6-11 days compared to the previous week’s 2-8 days. LSMGO requires lead times of 4-9 days, up from 2-6 days the previous week.

Biofuels

Rotterdam’s B30-VLSFO HBE bunker benchmark has gone up by $13/mt in the past week, while rallying LSMGO levels have pushed B30-LSMGO HBE up by a greater $25/mt.

The port’s B30-VLSFO UCOME benchmark has gone the other way, shedding $35/mt on the week and coming within $160/mt of HBE-rebated B30-VLSFO.

The Dutch HBE A ticket price has been highly volatile, peaking at around €23/GJ ($24.05/GJ) early last week before dropping to €17.50/GJ ($18.30/GJ) by Friday. This translates to a theoretical rebate of $163/mt for B30-VLSFO HBE blends sold in Dutch ports. While down from $210/mt a week ago, the rebate remains significantly higher than the $90/mt recorded in April.

In Singapore, an $18/mt gain for B24-LSMGO UCOME has been more than twice the $7/mt gain for B24-VLSFO UCOME.

Singapore remains a key market for Chinese UCOME cargo imports, with PRIMA Markets noting offers of UCOME FOB China in bulk at $1,020/mt on Friday. That was $180/mt lower than what a supplier indicated pure B100 UCOME at for bunkering in Singapore that day.

LNG

Rotterdam’s LNG bunker price has made a marginal rise of $4/mt to $853/mt – the highest it has been in over a year. The underlying front-month Dutch TTF Natural Gas contract settled at $13.92/MMBtu ($841/mt) on Thursday last week, a level not seen since October 2023.

A period of rising prices reflects growing concerns over gas supply stability in Europe, primarily due to the escalating Russia-Ukraine conflict, ING’s Warren Patterson said.

Singapore’s LNG bunker price has shot up by $37/mt to $889/mt. Colder temperatures have bolstered gas demand for heating and electricity in Japan. Production issues for Brunei LNG, a major producer in the region, has also supported the front-month NYMEX Japan/Korea Marker (JKM) contract, which influences price levels in Singapore’s LNG bunker market.

By Erik Hoffmann, Nithin Chandran and Debarati Bhattacharjee

Please get in touch with comments or additional info to news@engine.online