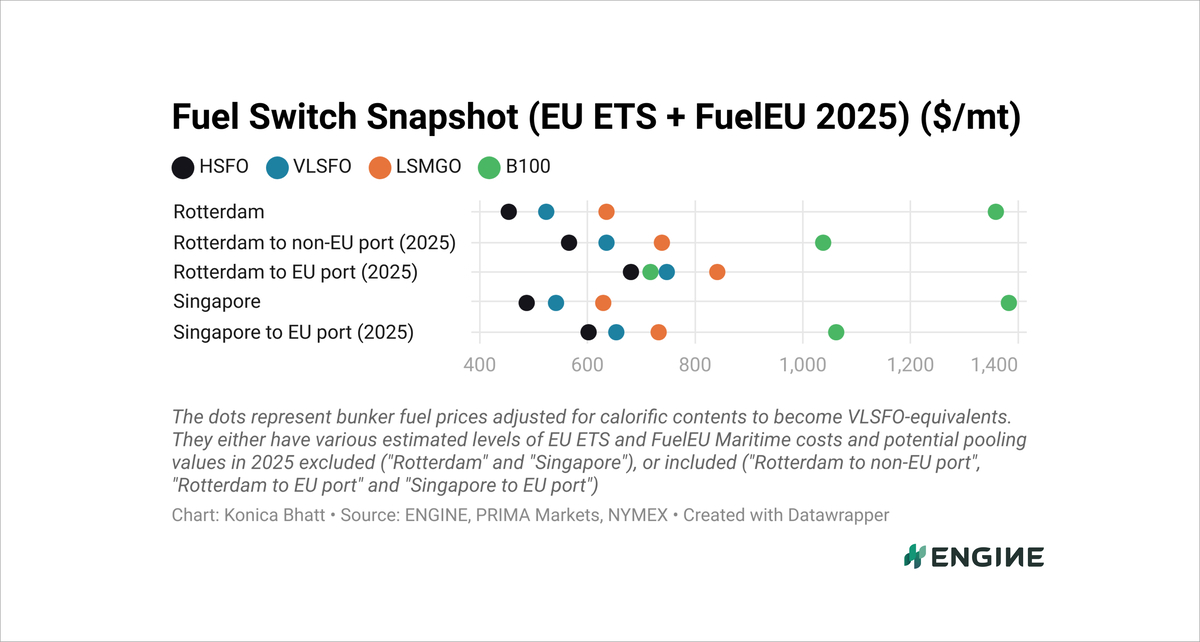

Fuel Switch Snapshot: Rotterdam’s B100 flips to premium over HSFO

B100 loses price advantage to HSFO, even with EU regs

LNG’s premium over VLSFO narrows

A sharp $46/mt increase in Rotterdam's VLSFO-equivalent price of B100 (100% biofuel) has pushed B100 to a $37/mt premium over conventional HSFO, from a $30/mt discount in the past week.

These prices include the cost impacts of EU Emissions Trading System (EU ETS) and FuelEU Maritime regulations. B100 is considered a zero-carbon fuel under EU ETS, while FuelEU penalises HSFO and rewards B100, which has a theoretical FuelEU pooling benefit of $642/mt. This reduces B100's estimeted real cost to $716/mt.

In comparison, HSFO’s real estimated bunkering cost has fallen to $680/mt in the past week, reflecting lower estimated EU Allowance (EUA) costs, and a $21/mt decline in the grade's VLSFO-equivalent price in the past week.

B100’s discount to Rotterdam’s VLSFO for intra-EU voyages has also narrowed sharply, dropping from $98/mt last week to $31/mt now.

Rotterdam’s VLSFO-equivalent LNG bunker price, including EU regulations, has dropped by $129/mt since 14 February, after a surge in European gas demand had briefly lifted the benchmark above $1,000/mt in early February.

As LNG prices ease down, the Rotterdam's LNG premiums over liquid fossil fuels have also narrowed.

The VLSFO-equivalent price of LNG in Rotterdam is now $158/mt higher than VLSFO when used in an Otto medium-speed (Otto MS) engine with a 3.1% methane slip, reflecting a $46/mt decline in its premium over the past week.

For LNG dual-fuel shipowners deciding between LNG and biofuels, LNG now costs $189/mt more than B100 in Rotterdam - a $112/mt reduction in its price premium over the past week.

All the prices mentioned above account for EU ETS compliance costs and FuelEU Maritime penalties or pooling benefits for voyages between two EU ports.

Liquid fuels

Rotterdam’s VLSFO price has declined $13/mt over the past week, closely tracking a $12/mt drop in the front-month ICE Brent futures contract. With EU regulations factored in, the decline is sharper at $21/mt. Prompt VLSFO supply remains tight in the wider ARA region.

Singapore’s VLSFO benchmark has fallen by a larger $30/mt in the same period.

This price decline seems to be largely driven by lower-priced stems recorded in ENGINE’s database for both prompt and non-prompt deliveries in the port. Recommended lead times have now been extended to 10 days, up from five days last week.

Liquid gases

Rotterdam’s VLSFO-equivalent LNG price has dropped $60/mt lower over the past week, or $67/mt when factoring in EU regulations. The decline has mainly been driven by a 14% plunge in the front-month Dutch TTF Natural Gas contract.

According to the Japan Organization for Metals and Energy Security (JOGMEC), the decline can mostly be attributed to “warm weather and discussions on the introduction of flexible gas storage targets.”

Singapore’s VLSFO-equivalent LNG benchmark has seen a smaller $15/mt decline, following a $0.33/MMBtu ($18/mt) decline in the NYMEX Japan/Korea Marker (JKM) benchmark.

“Progress in peace negotiations over the war in Ukraine and sluggish demand in Asia” seem to have weighed on the JKM benchmark, JOGMEC explained.

By Konica Bhatt

Please get in touch with comments or additional info to news@engine.online