Fuel Switch Snapshot: Rotterdam’s LBM and B100 prices extend declines

HBE rise drags B100 price lower in Rotterdam

LNG–VLSFO spread widens in Rotterdam

Singapore LNG narrows gap to VLSFO

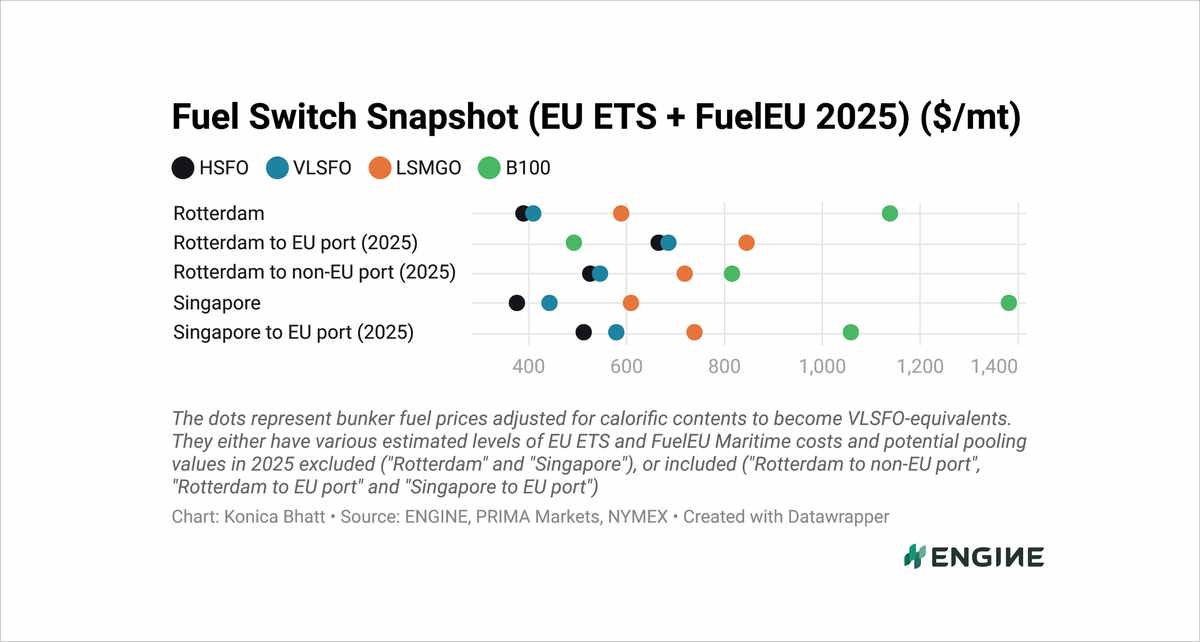

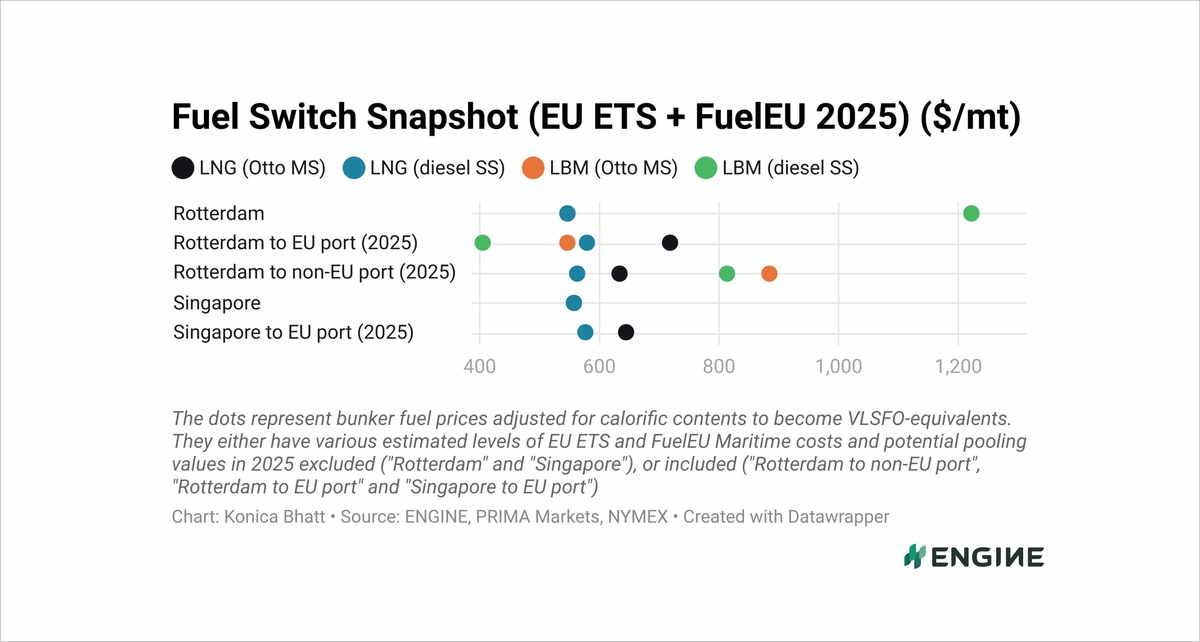

All bunker prices mentioned below have been adjusted for calorific contents to make them VLSFO-equivalent. They have estimated EU-EU voyage compliance costs included for Rotterdam, and non-EU-EU compliance costs included for Singapore. These account for EU ETS costs and FuelEU Maritime penalties, and our estimated compliance surplus values for FuelEU pooling. Rotterdam's B100 and LBM prices also factor in Dutch HBE rebates for advanced liquid and gaseous biofuels sold in the Netherlands.

All bunker prices mentioned below have been adjusted for calorific contents to make them VLSFO-equivalent. They have estimated EU-EU voyage compliance costs included for Rotterdam, and non-EU-EU compliance costs included for Singapore. These account for EU ETS costs and FuelEU Maritime penalties, and our estimated compliance surplus values for FuelEU pooling. Rotterdam's B100 and LBM prices also factor in Dutch HBE rebates for advanced liquid and gaseous biofuels sold in the Netherlands.

Rotterdam’s B100 discount to VLSFO has remained broadly steady, narrowing by just $1/mt over the past week to $191/mt. Its discount to LSMGO has narrowed by $17/mt to $352/mt.

For dual-fuel vessels, LNG is now priced $104/mt below VLSFO in Rotterdam when used in low-methane slip engines - a $9/mt wider discount than last week.

For vessels with high-methane slip engines, LNG is priced $36/mt above VLSFO, reflecting an $8/mt decline in the premium on the week.

In Singapore, LNG is now only $5/mt cheaper than VLSFO in low-methane slip engines, compared to a $40/mt discount a week ago. For high-methane slip engines, LNG carries a $65/mt premium over VLSFO, up $40/mt on the week.

Rotterdam's LBM discounts to fossil LNG have stayed unchanged at $173-177/mt for another week.

Liquid fuels

Rotterdam’s VLSFO price has dropped by $19/mt over the past week, while Singapore’s has fallen by a sharper $30/mt. Both benchmarks have largely tracked a $24/mt decline in the front-month ICE Brent futures contract.

A trader has recommended 5–7 days of lead time for VLSFO in the ARA region.

In Singapore, VLSFO lead times have continued to fluctuate, with some suppliers able to deliver in as little as six days, while others suggest booking up to two weeks in advance. A week ago, lead times ranged between 8–14 days.

Rotterdam’s B100 benchmark has declined by $18/mt in the past week, mostly weighed down by an $18/mt rise in the Dutch HBE rebate for marine B100.

Singapore’s B100 price has dropped by $17/mt on the week.

The port’s B100 sales decreased from an all-time monthly high of 4,800 mt in August to 4,500 mt in September.

Liquid gases

Rotterdam’s LNG bunker price has slipped by $27–28/mt in the past week, while its LBM price has fallen by a similar $26–27/mt, depending on engine type and methane slip.

LNG bunker sales in Rotterdam reached a record high of 122,000 mt in the third quarter. Combined LNG sales in the first three quarters were about 9% higher than the same period last year.

In contrast, Rotterdam's LBM sales dropped from 2,100 mt in the second quarter to just 400 mt in the third quarter.

Singapore’s LNG bunker price has remained largely stable, edging up by $5–6/mt on the week, depending on the vessel’s engine type.

The port’s LNG bunker sales declined from 67,000 mt in August to 48,000 mt in September.

By Konica Bhatt

Please get in touch with comments or additional info to news@engine.online