Q&A: Blue ammonia is a long-term option - Yara Clean Ammonia

Yara Clean Ammonia president Magnus Krogh Ankarstrand discusses whether the cost of producing clean ammonia can come down to match conventional marine fuels.

PHOTO: Yara's ammonia production plant on the Herøya peninsula near Porsgrunn, Norway. Yara

A growing number of shipowners and operators are exploring clean ammonia to reduce their fleets' future carbon footprints. Clean ammonia can either be produced from renewable electricity (green), or produced from natural gas with carbon capture during production (blue).

Despite the growing interest, the industry is concerned that green or blue ammonia will be prohibitively expensive alternatives to conventional fuels. Yara Clean Ammonia is the clean ammonia production arm of Yara International, one the leading ammonia producers in the world. It plans to make clean ammonia available for bunkering in Scandinavia at the beginning next year.

Yara has been developing what could become one of the world's first ammonia bunker and loading stations. It partnered with Norwegian bunker firm Azane Fuel Solutions on the project. Azane has ordered several of these stations and the idea is roll them out all over Scandinavia.

Yara Clean Ammonia president Magnus Krogh Ankarstrand talked to ENGINE and offered insights into the company's long-term price projections for ammonia and whether its blue or green form is most feasible.

Do you think blue ammonia is a long-term solution to decarbonise the maritime sector, or do you believe it is time to ramp up green ammonia production exclusively?

Blue ammonia is a viable long-term solution, mainly because at the end of the day all energy sources and energy carriers must be measured based on their carbon footprint. Green ammonia is expected to require significant premiums and subsidies to be competitive short-term due to high capital expenditures (capex), current electrolyser efficiency rates and competition for renewable electricity in grid-connected locations. Even if the renewable energy costs are fixed, the lack of access to renewable electricity will be a deterrent to significantly scaling up green ammonia production to meet growing global demand.

Do you think it will be more challenging to scale renewable electricity infrastructure than carbon capture technologies? Can it be considered cost-effective?

Absolutely, yes, 100%. When compared to renewable electricity, carbon capture technologies can be obtained at cost-competitive rates. In general, building the infrastructure required to generate large amounts of renewable electricity is very expensive. Additionally, the cost of electrolysers [to produce green hydrogen] is quite high, and current electrolysers have low energy efficiency [so they require more power to produce more hydrogen].

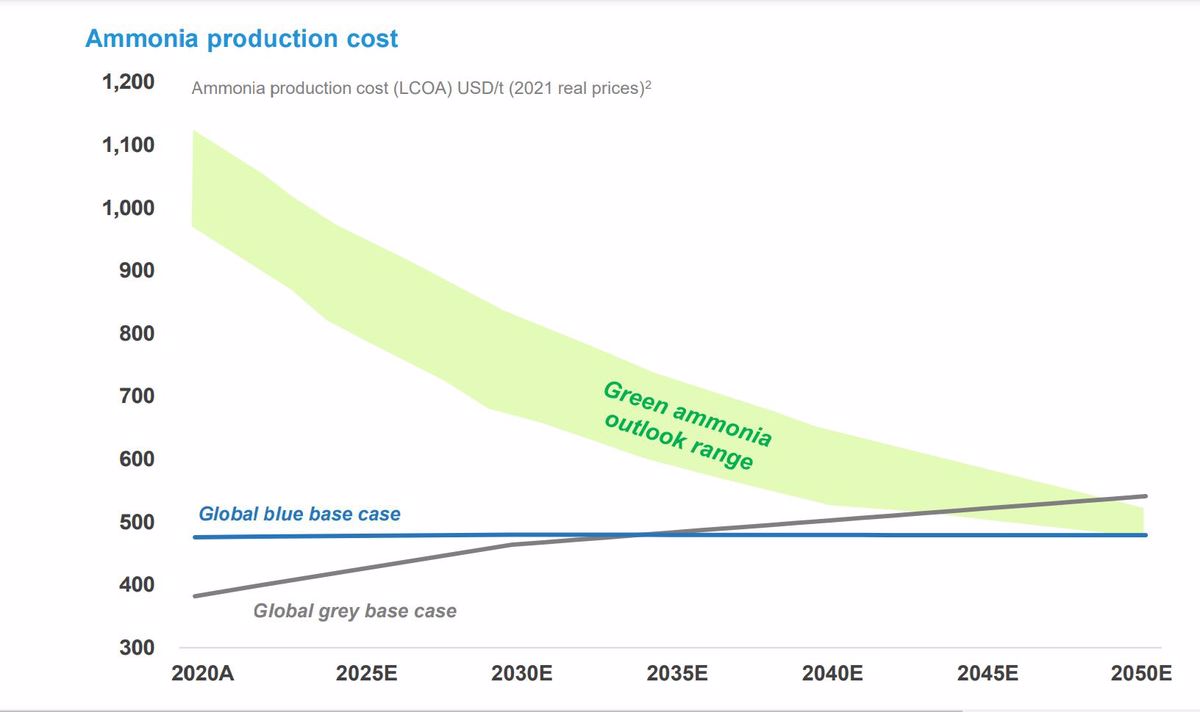

CHART: Yara's estimates for ammonia production cost from 2020-2050 as part of a Capital Markets Day presentation from 2022. Yara Clean Ammonia

Do you believe green ammonia will always remain at a strong price premium over blue and grey ammonia? Can their prices converge in the near future?

Green ammonia will prevail in the long term, as the total plant capex comes down and efficiencies and load factors increase as the industry develops, but it will take time until it becomes cost competitive without subsidies. I think we are talking 2050. A significant increase in the installation of solar or wind and scaling up electrolyser production to an industrial level will bring down the operating costs of green ammonia production.

What is your projection of the production costs for blue and green ammonia for the 2030s?

Currently, from a marginal cost of production perspective, green ammonia will be priced north of $1,000/mt. [Yara's projections indicate that the cost of producing green ammonia will almost halve to around $500/mt by 2040, and that electrolysis capex could come down 60-70% by 2040.]

Speaking of blue ammonia, from a marginal cost of production perspective, it is a bit difficult to assess the cost of blue ammonia, since blue ammonia is essentially grey ammonia almost without CO2. The current carbon tax rate across Europe is an average price of $87/mt of CO2 and that could rise to around $150-200/mt of CO2 in the coming years, so the blue ammonia price might be $100-200/mt higher than grey ammonia spot price to compensate for taxes. However, more demand for decarbonised ammonia, blue or green, will definitely drive the prices upwards.

Holistic view of fuel and emissions costs needed

Yara has estimated that carbon pricing of $250/mt is needed for ammonia to reach cost parity with the marine gasoil (MGO) prices – assuming prices of $750/mt for MGO and $500/mt for ammonia.

Shipowners should compare the cost of fuel based on the total cost of propelling their ships, Yara has said. Calculations should include the price of the fuel, its energy density and its efficiency during combustion in an engine.

Yara has also pointed out that the price of carbon will likely play an increasingly important role going forward. This means that a fuel's CO2 emissions and carbon intensity on a well-to-wake basis should also be considered in cost calculations.

By Konica Bhatt

Please get in touch with comments or additional info to news@engine.online