The Week in Alt Fuels: Trump’s pushback vs global tide

Shipping’s green fuel transition is already in motion. For nations and companies alike, it’s a chance to shape the market and share in the gains, not a contest with winners and losers.

IMAGE: ENGINE via ChatGPT

IMAGE: ENGINE via ChatGPT

The Trump administration’s recent threat to retaliate against IMO members that seek to adopt the Net-Zero Framework in October has sparked concern.

The framework would require ships to progressively cut the greenhouse gas (GHG) intensity of their fuels, with targets tightening towards 2035 and an ambition for a 65% reduction by 2040. This could eventually force a transition to low- and zero-emission bunkers across the global fleet.

Trump’s objections rest on two claims: China will benefit disproportionately from the alternative fuel transition and higher fuel costs and non-compliance penalties will raise energy, transport and leisure cruise prices.

These arguments overlook the diversity of the green fuel landscape and the tools already available to manage costs.

Not a ‘single-fuel, single-country’ story

Several shipping experts, including DNV, the Mærsk Mc-Kinney Møller Center for Zero Carbon Shipping and Lloyd’s Register, have repeatedly stressed that the industry’s future fuel mix will consist of multiple options rather than a single fuel.

This multi-fuel approach can be a great opportunity for all countries to participate, rather than becoming a single-nation story.

Yes, China has several green methanol plants in the pipeline and already in operation. But it is far from the only the only player in this space. As we noted in one of our earlier newsletters, the EU is emerging as a hotspot for bio- and e-methanol production with companies like Liquid Wind, European Energy, Repsol planning production across the continent.

Low-carbon variants of methane and ammonia are also in the running for shipping’s future fuel mix.

Liquefied biomethane (LBM) production is currently mostly concentrated in the EU. Countries like Finland are leading thanks to a well-developed gas grid and infrastructure. Across Europe, new plants and supply agreements are being developed to meet shipping’s rising demand.

Beyond LBM, large-scale green and blue ammonia and green methanol projects are advancing in India, Brazil, Spain and elsewhere. Even in the US, planned green fuel projects in Texas and along the Gulf Coast could put this region on the map as a production hubs of low- and zero-emission fuels.

Willing industry

Shipowners and operators are not shying away from the shift. Many global companies are proactively ordering alternative-fuel capable vessels and some have even started bunkering ammonia, which is considered to be technically demanding.

Their motivations seem to range from meeting regional regulations to securing charterer preference or positioning themselves ahead of future compliance deadlines.

In the EU, biofuel bunkering has picked up a steady pace and LBM is beginning to catch up. We have also seen methanol-capable container ships enter into service and ammonia-ready tankers on order. LBM supply contracts in Europe, green methanol bunkering in Amsterdam, Singapore and China and early ammonia tests and trials in China, Singapore, Australia, Rotterdam or and even India are all underway today – well before the IMO's global GHG intensity limits are in effect.

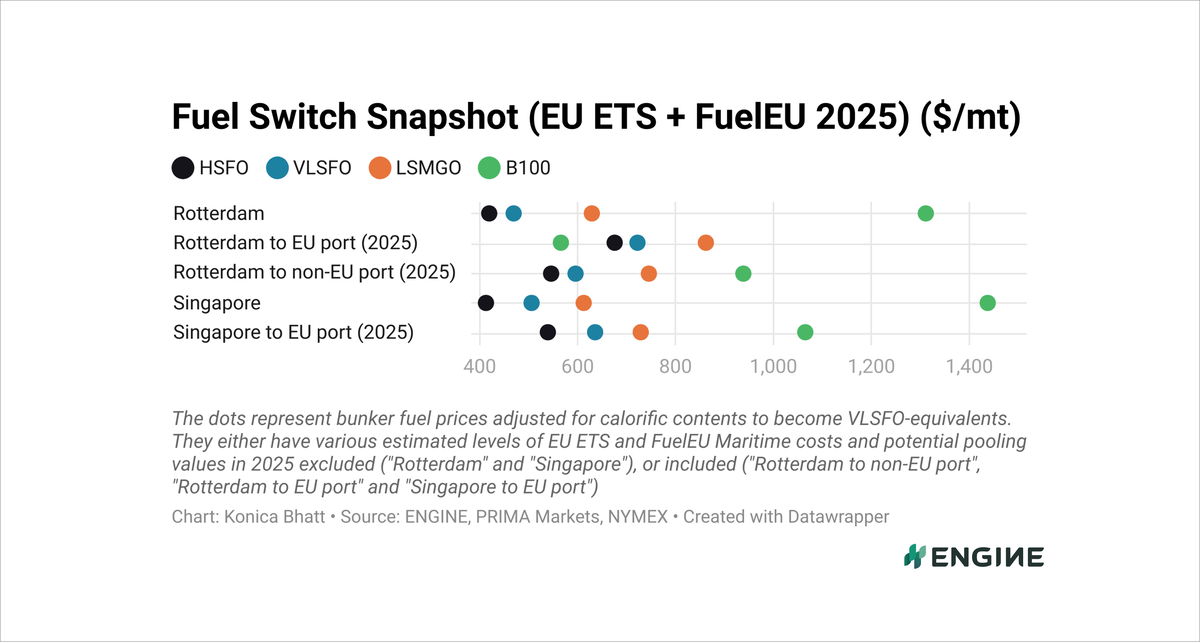

Cost challenges can be met – and shared

As we have seen in the EU, regulatory incentives and market mechanisms can make a real difference.

ENGINE’s analysis of vessels bunkering LBM and 100% biofuel (B100) in Rotterdam shows that combining the Dutch biofuel market incentive with FuelEU’s pooling mechanism and the EU Emissions Trading System (ETS) can significantly narrow the price gap with fossil fuels.

Pooling allows overcompliant ships to sell surplus compliance to underperforming ones in the same group, which can effectively offset the higher cost of bunkering alternative fuels. When layered with national incentives, the effect can be substantial.

Regulations are not the only alternative fuel drivers. Voluntary demand for green freight from cargo owners able to pass on costs is a sign that consumers are willing to foot slightly higher bills for goods. When the costs are spread out across thousands of goods, the extra cost per item is marginal.

For instance, the Zero Emission Maritime Buyers Alliance (ZEMBA) has contracted Hapag-Lloyd to use LBM on its vessels. Hapag-Lloyd will then allocate carbon credits to ZEMBA members based on the GHG reductions it achieves from its LBM-fuelled voyages between Europe and Asia. A book-and-claim mechanism will be used to redistribute these carbon credits.

This system allows major cargo owners to claim Scope 3 emission savings by paying premiums for carbon credits to Hapag-Lloyd and other shipping companies, even if their actual cargo is transported on other conventionally-fuelled vessels.

“Our members are demonstrating that freight buyers are willing to make multi-year advanced offtake commitments now to incentivize the creation of new markets for the most scalable solutions, which will be required for them to achieve their 2030 and 2040 climate goals,” ZEMBA’s chief executive, Ingrid Irigoyen explained.

ZEMBA members include Amazon, Nike, Meta, Patagonia and several other major global retailers.

“By creating economies of scale and targeting investment in the right long-term solutions, our members can also accelerate the pace and manage [the] overall costs of this clean energy transition,” Irigoyen added.

The choice ahead

The shift to low- and zero-emission fuels will certainly come with challenges. Infrastructure must scale, supply chains must adapt and costs must be managed. But the course is set. Technology is advancing, projects are underway and the industry is engaged.

Even if some countries resist, the IMO framework will be enforced through port state controls, which means that it will apply in countries that have ratified MARPOL. Ships calling at those ports will have to comply, regardless of their flag state’s stance.

This leaves policymakers and industry leaders with a clear choice: engage with the change, help shape it and capture the opportunities it offers; or stand aside and let others lead.

The green fuel transition is not a zero-sum game. All countries have the opportunity to drive the shift andshare in its gains. But early movers will set the rules, build markets and develop expertise, while latecomers will simply have to comply or become pariahs. The question now is no longer whether shipping’s transition will happen, but who will be ready to benefit when it does.

In other news this week, L&T Energy GreenTech, a subsidiary of Indian conglomerate Larsen & Toubro, will develop a 300,000 mt/year green ammonia plant at the Kandla Port in Gujarat, India. Japanese conglomerate Itochu will offtake the entire production and offer it as bunker fuel in Singapore.

Van Oord has completed its first LBM bunkering in Elbe, Germany. The Dutch offshore construction firm's dredging vessel Vox Ariane was bunkered with LBM, which it says is a key part of its long-term net zero strategy.

Golden Island’s bunker vessel has arrived in Singapore to begin bio-methanol bunkering trials in the world’s busiest bunkering port. The vessel will offload part of its cargo at the port's Stolthaven Terminal on 15 August, while the remaining fuel will be kept onboard for an acceptance test to assess compatibility with Singapore’s methanol bunkering regulations.

By Konica Bhatt

Please get in touch with comments or additional info to news@engine.online