Bio-bunker demand wanes in Singapore and China

Bio-bunker demand drops in Singapore

B24-VLSFO very tight in China

EU imports less Chinese UCO

PHOTO: Vopak recently commissioned 40,000 cbm of capacity at its Sebarok terminal for blending biofuels into marine fuels. Vopak

PHOTO: Vopak recently commissioned 40,000 cbm of capacity at its Sebarok terminal for blending biofuels into marine fuels. Vopak

Changes in weekly bio-blend prices:

- Singapore's B24-VLSFO up by $4/mt to $737/mt

- Singapore's B24-LSMGO up by $5/mt to $847/mt

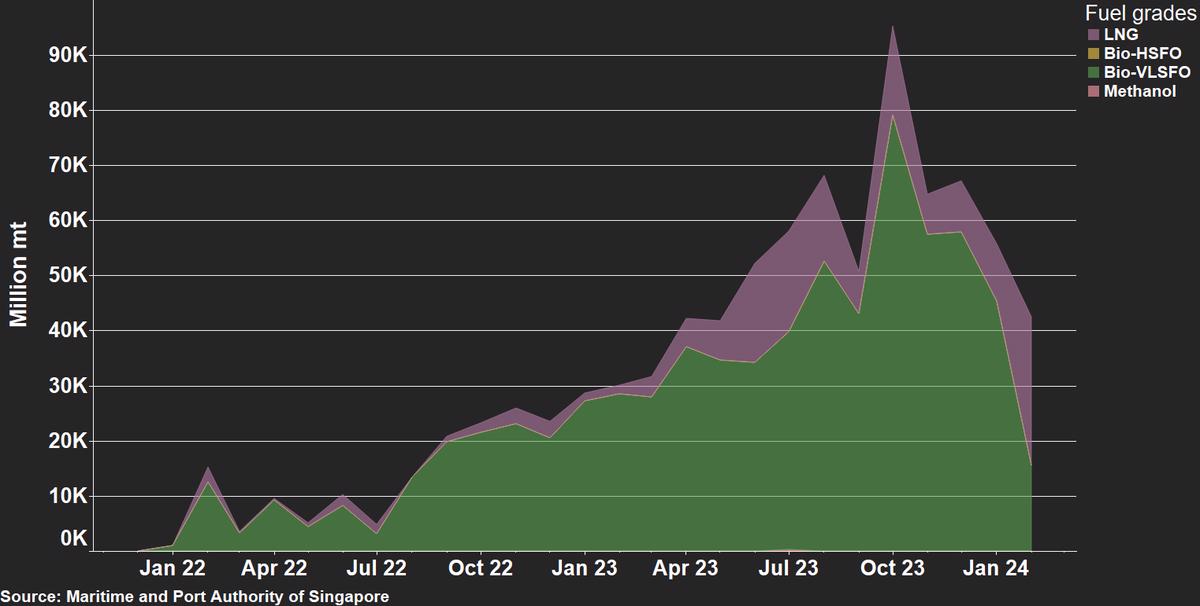

Demand for B24-VLSFO has been slow in Singapore, sources say. Recent bio-blended bunker sales data from Singapore’s port authority also reflects the slowing demand trend. Only 16,000 mt of bio-VLSFO (mostly B24) was sold in Singapore in February, which was the least since August 2022.

CHART: Bio-VLSFO sales have grown sharply in Singapore over the past two years and peaked late last year, before slumping since. Maritime and Port Authority of Singapore

CHART: Bio-VLSFO sales have grown sharply in Singapore over the past two years and peaked late last year, before slumping since. Maritime and Port Authority of Singapore

Shipowners are increasingly adopting technologies like air lubrication and bubble systems to enhance vessel’s efficiency and get a lower Carbon Intensity Indicator (CII) rating, a source says. This shift towards efficiency technologies, which are often one-off investments, is evidently favoured by some over bunkering bio-blends in ports like Singapore.

Several suppliers in Singapore determine their B24-VLSFO prices by adding a biofuel premium to the price of the VLSFO component, which is typically based on a FOB VLSFO cargo price. These premiums have decreased from $220/mt in the latter part of last year, through $180/mt at the beginning of this year, to around $150/mt now.

Lead times of up to seven days are generally recommended for B24-VLSFO in Singapore. But these deliveries are subject to barge availability as only a few barges carry the product, a trader says.

Similarly, mainland China is experiencing slow demand. Not many B24-VLSFO stems have been booked in Chinese ports in recent weeks. B24-VLSFO is almost out of stock in Zhoushan, China's biggest bunker port. Some can offer B24-VLSFO in the port, but these deliveries are subject to firm enquiries and product availability. This is partly because VAT is not waived for biofuel blends, which discourages Chinese refiners and blenders from blending them with VAT-exempt VLSFO.

The scenario has been slightly different in Hong Kong, where bunker supplier Chimbusco Pan Nation (CPN) has delivered a couple of B24-VLSFO stems in recent weeks, among them a stem delivered to a container ship earlier this month.

Upward pressure:

Shipments of palm oil mill effluent (POME) from Indonesia have faced challenges because of the ongoing tensions in the Red Sea. Freight rates from Indonesia to European countries have increased significantly, as vessels avoid passage through the Suez Canal and opt for longer voyages around Africa.

Despite these logistical challenges, demand for ISCC-certified POME from Indonesia has been strong over the past three weeks, Indonesian waste-based biofuel firm Beli Jelantah’s founder Faris Razanah Zharfan told ENGINE. POME is a waste-based feedstock that is collected from palm mills during processing.

Some of these POME exports are heading for the Netherlands, Zharfan explained. It is likely that some suppliers and blenders in Rotterdam are using POME sourced from Indonesia for marine biofuel blending. Rotterdam is the biggest biofuel bunkering hub in terms of volumes sold, and POME-based biofuel blends can qualify for Dutch price rebates, making it an attractive feedstock for biorefiners, blenders and bunker suppliers there.

Going forward, the ongoing Red Sea crisis and high freight rates may make it more expensive for Dutch buyers to import POME cargoes from Indonesia. This could have a knock-on impact to increase prices for biofuel blends in Rotterdam and nearby ports.

Downward pressure:

Chinese UCO exports to the US and European countries have dropped amid supply of cheaper local alternatives and logistical challenges in the Red Sea, according to PRIMA Markets. Lacklustre demand from key markets such as the EU and the US could lead Chinese UCO prices to decline and potentially lower Singapore's B24-UCOME prices, as the country imports significant volumes of UCOME from China.

UCO is typically reacted with methanol as a catalyst to produce used cooking oil methyl ester (UCOME). Bids for UCO FOB China in bulk were seen at $805/mt on Tuesday against offers of $825/mt, data from PRIMA Markets shows.

“For sure, Chinese UCO export to the EU have slowed down. However, exports to the US are still going strong,” Zharfan argued. Biodiesel refineries in the US are still reliant on Chinese UCO imports to meet refinery capacity needs, and UCO imports from China are the only viable option in terms of quantity, he added.

Indonesia is an alternative UCO exporter that could fulfill US import needs, but Indonesian suppliers are still working to meet supply traceability paper requirements for UCO exports, Zharfan noted. Other factors, that could influence Chinese UCO exports to the US will be a drop in renewable identification number (RIN) values, he said.

When a biofuel batch is produced, a RIN is generated and assigned to it. The RIN specifies information like the type of biofuel and the feedstock used to produce it, and these RINs can be bought or sold in the open market.

A bipartisan bill was recently put forward to the US Senate, which argues for suppliers to get RIN credits for selling biofuel bunker blends to ocean-going vessels.

By Nithin Chandran

Please get in touch with comments or additional info to news@engine.online