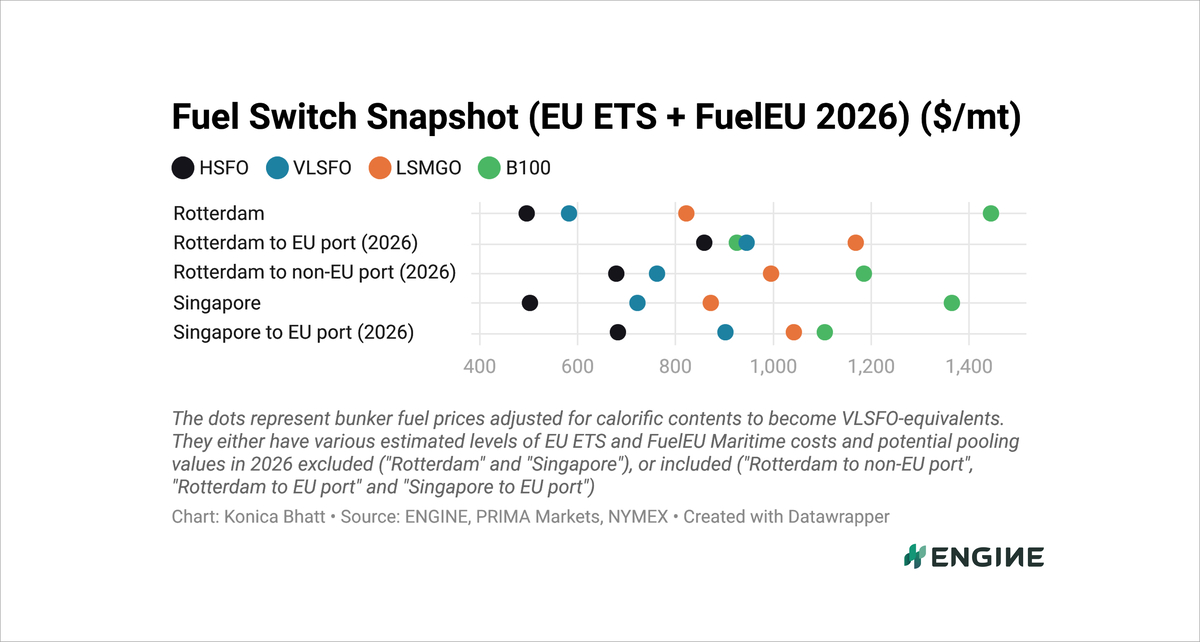

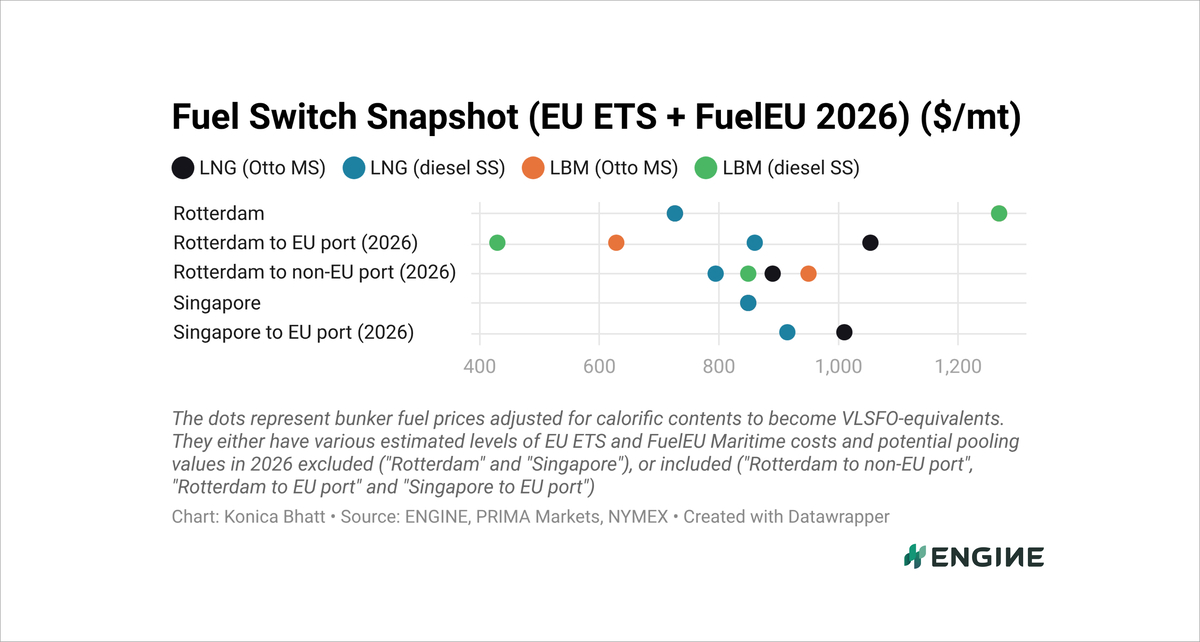

Fuel Switch Snapshot: Lower surplus prices dent B100 and LBM pooling values

OceanScore’s FuelEU Pooling Index drops to 2026 low

B100’s discount to VLSFO narrows to $18/mt

LBM pooling values lose up to $306/mt since May

All bunker prices described in the text below have been adjusted for calorific content to make them VLSFO-equivalent. They have estimated EU-EU voyage compliance costs included for Rotterdam, and nonEU-EU compliance costs included for Singapore. These account for EU ETS costs and FuelEU Maritime penalties, and the average price of compliance surpluses we have picked up from the FuelEU pooling market from the past week.

All bunker prices described in the text below have been adjusted for calorific content to make them VLSFO-equivalent. They have estimated EU-EU voyage compliance costs included for Rotterdam, and nonEU-EU compliance costs included for Singapore. These account for EU ETS costs and FuelEU Maritime penalties, and the average price of compliance surpluses we have picked up from the FuelEU pooling market from the past week.

OceanScore's FuelEU Pooling Index has fallen to €169/mtCO2e ($193/mtCO2e) this week, its lowest level of the 2026 compliance cycle so far.

The benchmark has declined by €4/mtCO2e ($5/mtCO2e) over the past week. Over the same period, ENGINE-assessed FuelEU Maritime pooling values for B100 and liquefied biomethane (LBM) on EU-EU voyages have fallen by $20/mt and $29-33/mt, respectively.

While the weekly decline in pooling values has been relatively modest, the impact is more pronounced over a longer period. Market participants shifted their focus to 2026 FuelEU compliance in May after completing 2025 reporting and pooling activities by the end of April.

Since the first week of May, OceanScore's FuelEU Pooling Index has slumped by €56/mtCO2e, from €225/mtCO2e ($263/mtCO2e) to €169/mtCO2e ($193/mtCO2e) now.

The decline in the underlying benchmark has reduced B100's potential pooling value by $188/mt to $522/mt over the same period.

LBM pooling values have been hit even harder, falling by $261-306/mt to $724-849/mt.

“The decline suggests that sellers are becoming increasingly willing to place compliance surpluses at lower price levels than earlier in the year, and a belief that banking will not translate into better prices any time soon,” OceanScore said.

The decline in pooling values has impacted bunker spreads in Rotterdam.

On 5 May, Rotterdam's B100 stood at a $299/mt discount to HSFO. That has since shifted to a $68/mt premium over HSFO. Its discount to VLSFO has narrowed by $395/mt to $18/mt and its discount to LSMGO has narrowed by $622/mt to $240/mt.

LBM discounts to LSMGO have narrowed by $469-509/mt, and to LNG by $132/mt over the same period.

Liquid fuels

Rotterdam's conventional fuel prices have fallen by $32-102/mt over the past week, while its B100 price has edged up by $1/mt.

Prompt HSFO and VLSFO availability remains tight in the ARA bunkering hub, because of loading delays at the terminals, a trader said. Lead times of around 7-8 days are recommended for both grades.

Singapore’s HSFO and LSMGO prices have declined by $18-78/mt in the past week, while its VLSFO price has risen by $34/mt. Its B100 has declined by $29/mt.

VLSFO availability in Singapore is still facing constraints, with suppliers recommending lead times of 10-14 days for deliveries.

HSFO availability has improved marginally, with lead times shortening to 5-12 days from 10-15 days previously. LSMGO availability has become more stretched, requiring 7-10 days of advance planning versus roughly seven days previously.

Liquid gases

Rotterdam’s LNG prices have declined by $27-33/mt in the past week. The LBM price for Otto medium-speed engines has inched lower by $2/mt, while the price for diesel slow-speed engines has inched higher by $3/mt.

Singapore’s LNG prices have plunged by $150-153/mt on the week.

By Konica Bhatt

Please get in touch with comments or additional info to news@engine.online